Sponsored – Est. Read 8 Min

America’s Highest-Grade Lithium Clay Deposit Appears to Offer Significant Upside Potential

With a higher-grade deposit, lower projected costs and a $24 billion mining major already on board, Surge Battery Metals (TSXV: NILI); (OTCQX: NILIF) may be the most overlooked lithium story in America today.

For more than a decade, America imported the lithium it needed.

That’s no longer an option.

The U.S. faces a structural lithium shortage that widens every year through 2040.

Battery factories are coming online from Tennessee to Nevada, EV adoption keeps climbing, and grid-scale battery storage has now overtaken EVs as the fastest-growing source of lithium demand globally.

“Lithium prices are ticking up again…Strong EV growth in China is playing a major role…but growth in stationary storage, batteries for the grid, is also contributing to rising demand for lithium in both China and the US.”

Washington has put domestic supply at the top of the national security agenda, with billions of dollars now flowing to projects that can produce critical minerals on American soil.

The most advanced of those projects is Thacker Pass. Located in northern Nevada, this project has already raised more than $3 billion to advance, including a $2.23 billion loan from the U.S. Department of Energy, $945 million from General Motors and $250 million from Orion. The mine is targeted to enter production in 2028 after a 2027 commissioning period.

Once Thacker begins producing in 2028, the question of whether U.S. lithium clay can be mined economically goes away.

And as Thacker Pass moves toward production, the prospects for another U.S. lithium project continue to impress.

It’s a project located in Nevada…and it’s following Thacker’s exact path right now. This project is on the same type of deposit and the same type of process chemistry as Thacker Pass…and with a higher-grade resource sitting right at the surface.

That project is the Nevada North Lithium Project. And it’s owned by Surge Battery Metals (TSXV: NILI); (OTCQX: NILIF).

ANALYST REPORT:

“We believe Surge is mispriced on both a project-relative and asset-class-relative basis”

Here’s what makes the upside potential for Surge Battery Metals so interesting:

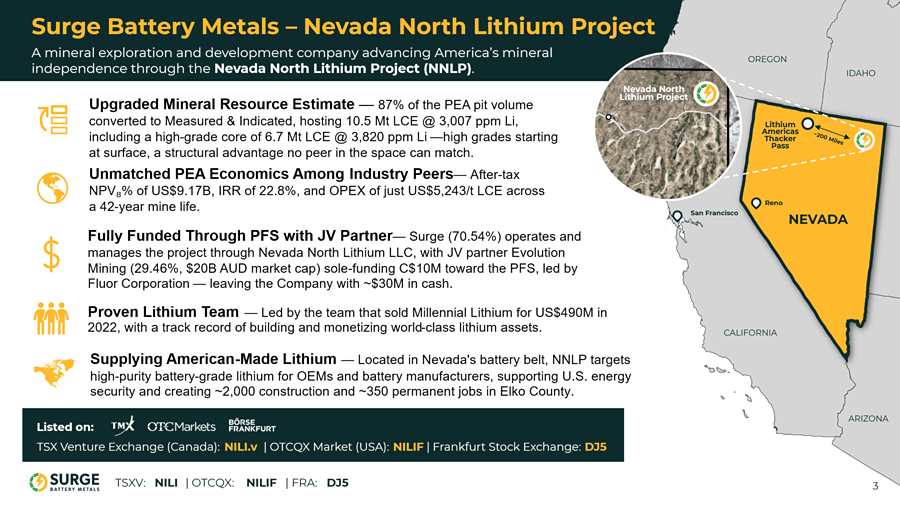

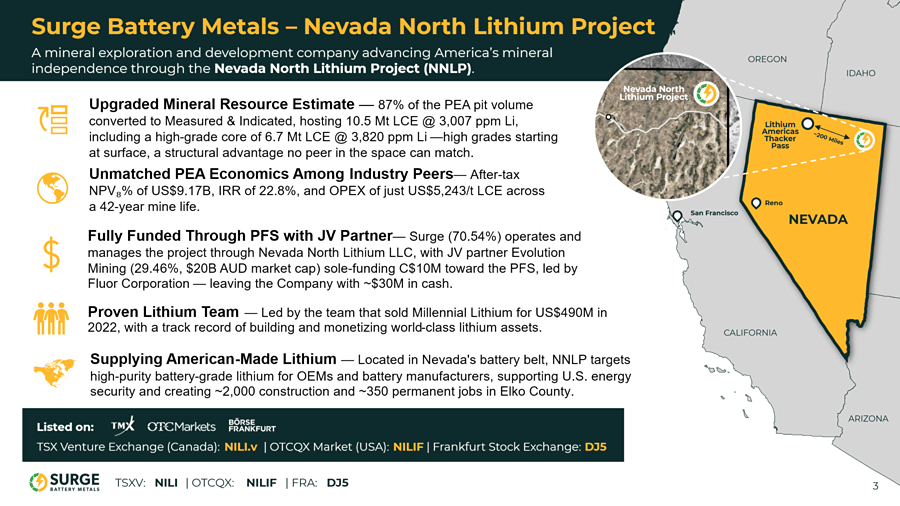

With the Nevada North Lithium Project, Surge holds the highest-grade lithium clay deposit in the United States.

The current resource stands at 10.51 million tonnes of Lithium Carbonate Equivalent (Measured and Indicated Mineral Resource[ii]) grading 3,007 ppm Li, roughly 50% higher than Thacker Pass.

The bulk of that resource sits at or near the surface, which means less stripping, less waste rock and lower operating costs once the mine is producing.

A Preliminary Economic Assessment delivered in 2025 projected an after-tax NPV of $9.17 billion, an IRR of 22.8% and operating costs of just $5,243 per tonne of LCE.

That puts Surge among the lowest-cost lithium producers anywhere in the world.

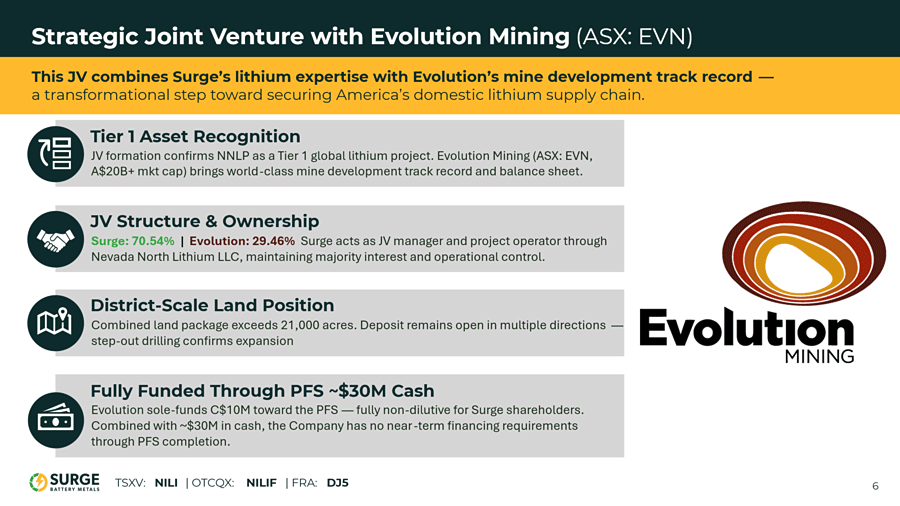

In September 2025, Evolution Mining (ASX: EVN), a global mining major with a market cap of roughly A$24 billion, signed a joint venture to fund Surge’s Pre-Feasibility Study. Surge remains the operator.

In addition, the team leading the way for Surge sold their last lithium project, Millennial Lithium, to Lithium Americas for US$490 million in 2022.

Thacker has proven that a U.S. lithium clay project can attract billions of dollars in capital and ride that funding to a multi-billion-dollar valuation.

Surge holds a higher-grade version of that same deposit, in the same state, using the same extraction approach, with stronger projected economics and a JV partner already funding the path forward.

The same path that took Thacker to a multi-billion-dollar market cap is the one Surge is working from today, with a few meaningful advantages of its own.

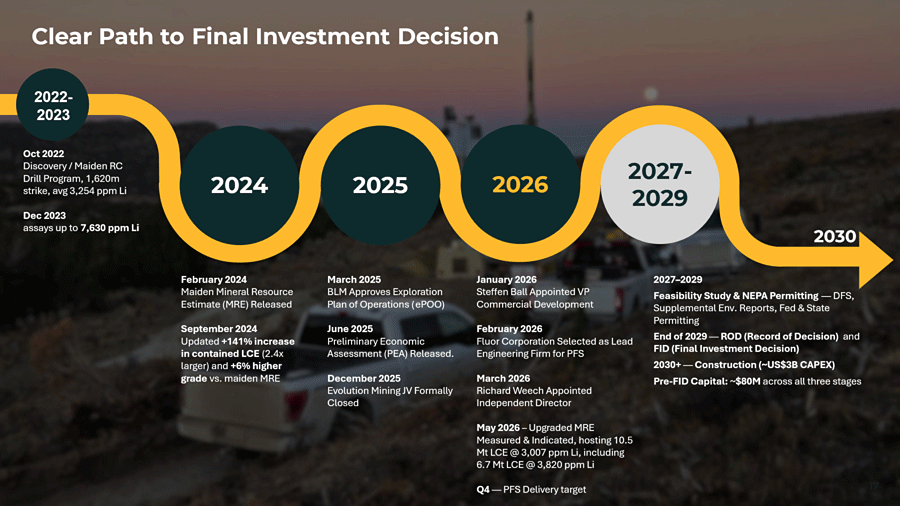

MRE UPGRADE: A WATERSHED MOMENT FOR NEVADA NORTH

M&I Resource: 10.5 Mt LCE @ 3,007 ppm Li | High-Grade Core: 6.7 Mt LCE @ 3,820 ppm Li

87% of the PEA pit volume converted to Measured & Indicated in just nine drill holes — one of the highest conversion ratios in the lithium clay sector, confirming exceptional deposit continuity.

- Grade improves with confidence — M&I grades increased at elevated cutoffs versus the prior Inferred estimate

- Deposit keeps growing — new M&I resource defined outside the original PEA pit, plus 3.1 Mt LCE Inferred extending the footprint further

- PFS fully de-risked — Fluor now has the high-confidence foundation to finalize mine design and capital estimates, with PFS delivery targeted Q4 2026

“Delivering over 10.5 million tonnes of LCE into M&I at grades exceeding 3,000 ppm Li places Nevada North in a league of its own.” — Greg Reimer, President & CEO, Surge Battery Metals

Here’s a closer look at why you should give Surge Battery Metals (TSXV: NILI); (OTCQX: NILIF) a closer look right now.

7 Reasons

Why You Should Strongly Consider Surge Battery Metals (TSXV: NILI); (OTCQX: NILIF) Today

1

The Highest-Grade Lithium Clay Deposit in America…Right at the Surface

Grade is the single most important driver of value in any lithium project. And on grade, Surge Battery Metals stands above the U.S. field. The Nevada North Lithium Project hosts 10.51 million tonnes of Lithium Carbonate Equivalent (Measured and Indicated Mineral Resource[iii]). The PEA mine plan grades average 4,016 ppm Li over the 42-year mine life — nearly double the Thacker Pass average of 2,200 ppm. Higher grade means more lithium recovered per tonne of material processed and lower processing costs. The geology offers a second advantage. The bulk of Surge’s resource sits at or near the surface. Thacker’s higher grades are buried deeper, requiring more stripping and blending. Surge can mine its highest-grade ore directly from the surface, which means less waste, lower production costs and stronger margins.

Not All Lithium Deposits Are Equal — Only the Best Get Built.

Across every lithium type — hard rock, brine, DLE, and clay — only the highest-quality, lowest-cost assets will achieve sustained, long-term production. Grade, scale, cost, and deposit continuity determine which projects get built and which ones don’t. The market rewards asset quality, not asset class.

Tier 1 assets — large scale, long mine life, low cost, high margins — get built first and operate through cycles. Nevada North Lithium Project is a clear Tier 1 lithium asset: the highest-grade lithium clay resource in the United States, near-surface and free-dig, with an estimated OPEX of US$5,243/t — delivering a 78% operating margin at $24,000/t LCE — a 42-year mine life, 86,000 tonne per year production scale, and fewer permitting and ESG constraints than peer projects.

NNLP is the leading clay lithium project in North America and is positioned for long-life, low-cost, high-margin production.

2

Following a Proven Blueprint That’s Already Attracted $3 Billion in Capital

The single biggest question facing any new lithium project in North America is whether its extraction method will work at commercial scale. That’s the open question for almost every Direct Lithium Extraction (DLE) project in the country…and none of them have proven the technology at full production yet. The Nevada North Lithium Project, as a clay deposit, doesn’t face that question. Surge’s project uses the same type of process chemistry and the same type of sedimentary clay deposit as Thacker Pass, which has already raised more than $3 billion to advance, including $2.23 billion from the U.S. Department of Energy, $945 million from General Motors and $250 million from Orion. Thacker is targeted to begin production in 2028 after a 2027 commissioning period. When it does, it validates the entire sedimentary clay category. And Surge Battery Metals will be the next major project in line.

3

A $24 Billion Mining Major Is Funding the Next Stage of Development

In September 2025, Evolution Mining (ASX: EVN), a global mining major with a market cap of roughly A$24 billion, signed a joint venture to advance the Nevada North Lithium Project. Evolution committed up to C$10 million to fund Surge’s Pre-Feasibility Study. Surge retains operatorship and a 70.54% stake. Strategic backing of this kind is massive at this stage of development. Major mining companies do extensive technical and financial due diligence before committing capital, and Evolution’s commitment signals that Surge’s Nevada North Lithium Project passed that test. Evolution has also indicated it will help introduce Surge to global banks and institutional investors once the PFS is delivered, which is targeted for Q4 2026. For shareholders, the partnership reduces near-term dilution risk and adds a heavyweight voice to the Surge Battery Metals story.

4

Built to Produce Lithium Cheaper Than Almost Anyone Else

In lithium production, costs are everything. A project that can produce cheaply makes money in any market, while a project that has higher costs gets shut down as soon as prices begin to dip. Surge’s Preliminary Economic Assessment, released in 2025, projects operating costs of just $5,243 per tonne of lithium carbonate equivalent. Thacker Pass, the most advanced lithium clay project in the country, projects operating costs of $8,039 per tonne. That’s a 35% cost advantage for Surge that compounds over a 42-year mine life. The same PEA shows an after-tax NPV of $9.17 billion at $24,000 LCE, a 22.8% IRR and a 4.7-year after-tax payback. Those are the kinds of numbers that get a lithium project built. They’re also the kinds of numbers that are more likely to attract strategic partners and offtake buyers.

5

A 42-Year Mine Plan That Uses Only 30% of the Resource

Most lithium projects have a single mine life and a clear endpoint. Surge’s Nevada North Lithium Project is built on a different scale entirely. The PEA outlines a 42-year mine plan that processes only 30% of the current resource. The remaining 70% offers decades of additional production potential beyond the initial mine life. This makes Nevada North a true multi-generational asset. And it also gives Surge room to scale production over time as demand grows, without ever running short on feed material. A 10.51-million-tonne LCE resource (Measured and Indicated Mineral Resource[iv]) with decades of upside beyond the mine plan puts Surge in rare company.

6

The Same Team That Sold Millennial Lithium for $490 Million

In lithium development, plenty of projects look good on paper…but far fewer ever get built. Surge’s team has successfully done this before. Chairman Graham Harris founded Millennial Lithium and sold it to Lithium Americas for US$490 million in 2022. He brought core members of that team with him to Surge, including Director Iain Scarr – who brings over 30 years of experience from Rio Tinto – and metallurgy expert Dr. Vijay Mehta, who brings over 50 years of industry experience and specializes in the technological and economic feasibility of battery-grade lithium brine processing. Surge has also added Steffen Ball, formerly of Nissan North America and Ford Motor Company, to drive OEM and offtake conversations. And Richard Weech, who led Berkshire Hathaway Energy’s renewables and lithium investments from 2014 to 2022, joined the board in early 2026 as an independent director. Resumes like these don’t show up at junior lithium companies by accident.

7

Made-in-America Lithium, Right When Washington Wants It Most

The United States imports more than 95% of its lithium, primarily from China and Chinese-controlled operations in South America and Africa. That kind of dependency is no longer politically acceptable. Washington is now putting billions of dollars behind projects capable of producing critical minerals on American soil. Thacker Pass alone secured a $2.23 billion loan from the U.S. Department of Energy. Surge’s Nevada North Lithium Project sits in the heart of this push, in the most established mining jurisdiction in North America, with infrastructure, a skilled workforce and a regulatory framework built for resource development. Surge is not yet eligible for federal financing because it remains pre-PFS…but as the company advances toward feasibility, it may become eligible for the same kind of project-boosting government support Thacker received.

Surge is not waiting for Washington to come to it. The company has engaged Cassidy & Associates, a Washington, D.C.-based government relations firm, to represent Surge Battery Metals in federal and agency outreach.

This engagement covers four priorities: building direct relationships with government agencies to align Nevada North with national critical minerals and energy security priorities; engaging on the ‘Unleashing American Energy’ executive orders to position Surge as a trusted domestic mineral production partner; pursuing funding pathways including critical mineral grants and loans as non-dilutive capital to accelerate NNLP development; and working with regulators, agencies, and industry coalitions to streamline permitting with the Department of the Interior.

As Greg Reimer, President and CEO, has stated: ‘Our engagement with Cassidy & Associates provides us with a respected voice and strengthens our ability to connect with agencies, policymakers, regulators, and industry partners who share our vision to build a secure battery materials supply chain.’

The Lithium Market Just Turned.

This Time the Math Is Different.

For the past two years, lithium was a bear market story. Prices crashed from over $80,000 per tonne in late 2022 to under $10,000 by mid-2025. Projects got shelved, developers pulled back capex, and the whole sector went quiet.

That story is over.

Spot lithium prices are climbing again. UBS just raised its 2027 forecast by 148%[v]. Barrenjoey lifted its 2026 number by 64%. Scotiabank told clients in January that the rally is “only the first leg in what should be a multi-year tightening cycle.[vi]” Morgan Stanley sees more upside ahead, citing demand from energy storage that has consistently surprised to the upside.

Behind those calls is a simple supply-demand problem.

Global lithium demand is projected to reach 3.7 million tonnes of LCE by 2030, more than double the 2024 level[vii] as EV adoption keeps climbing. In addition, battery energy storage is now growing close to 50% a year and could account for nearly a third of total battery demand by the end of the decade.

Meanwhile, supply growth has slowed, with Chinese production disrupted by mining audits, African projects still years from scale and Nevada developments facing permitting timelines measured in decades.

The result is a market that is moving from surplus to deficit and staying there. UBS, Barrenjoey and multiple other research desks now project structural deficits running through 2030 and beyond.

For the United States, the situation is sharper still.

The U.S. imports more than 95% of its lithium, the bulk of it from China or Chinese-controlled operations. Battery factories are coming online from Tennessee to Nevada. EV adoption is rising. But none of that can work without a domestic lithium supply chain.

Washington has responded with a mix of executive orders, DOE loan guarantees and producer tax credits, all aimed at moving lithium production back inside U.S. borders.

That’s the environment Surge Battery Metals (TSXV: NILI); (OTCQX: NILIF) is operating in. And it has the asset to match.

A True Generational Asset…Right Here in the United States

Most lithium projects are built to last a decade. Nevada North is built to last a lifetime.

The PEA outlines a 42-year mine plan — a generational asset that will still be producing domestic lithium long after today’s battery factories have been built, expanded, and rebuilt again. This is not a project designed to catch a commodity cycle. It is infrastructure. The kind America builds once and depends on for generations.

“Lithium Discovery Could Reshape U.S. Supply”

— U.S. Geological Survey[ix]

The USGS made national headlines with a lithium discovery containing 2.3 million tonnes. Nevada North already hosts more than four times that amount — and unlike a newly discovered deposit, Nevada North has a completed Preliminary Economic Assessment, a Pre-Feasibility Study underway with Fluor Corporation, and a 42-year mine plan ready to be built.

“A 42-year domestic lithium supply — built in America, for America.”

For decades, the United States has sent billions of dollars overseas to buy lithium from Chile, Argentina, Australia, and China. Every battery in every American EV, every grid storage system, every military drone and defense system has depended on a supply chain that runs through foreign governments and foreign companies.

That dependency is a national security vulnerability — and Washington knows it.

Nevada North changes the equation. A domestic mine with a 42-year life means American battery factories can source lithium from American soil, under American regulation, with American workers — for the next four decades.

“The United States had one sole producer of lithium and relied on imports for more than half the lithium used last year.”

— U.S. Geological Survey[ix]

Nevada North is designed to be part of the solution — not just for today’s demand, but for the generation of demand that comes after it.

Development of the Nevada North Lithium Project is expected to create approximately 2,000 construction jobs and 350 permanent operational positions — skilled, well-paying American jobs in one of the most established mining jurisdictions in the country. These are not temporary positions. They are careers. The kind of long-term employment that comes from building something that lasts 42 years.

Lithium is not just a battery material. It powers computers, military equipment, electric vehicles, phones, electric tools, and grid-scale energy storage. The USGS lists it as a critical mineral. The Pentagon depends on it. American manufacturers need it. And right now, America does not produce enough of it.

Nevada North is not just a mining project. It is an act of mineral independence.

Nevada North: America’s Highest-Grade Lithium Clay Deposit

The Nevada North Lithium Project sits in Nevada’s Elko County…and Nevada is the most established mining jurisdiction in North America, with infrastructure, a skilled workforce and a regulatory framework built for resource development.

It’s also where most of the meaningful U.S. lithium activity is happening right now.

What makes Nevada North stand out is grade.

The current resource estimate stands at 10.51 million tonnes of Lithium Carbonate Equivalent (Measured and Indicated Mineral Resource[x]). The PEA mine plan grades average 4,016 ppm Li over the 42-year mine life — nearly double the Thacker Pass average of 2,200 ppm.

That makes the Nevada North Lithium Project the highest-grade lithium clay deposit in the United States by a wide margin.

Most U.S. clay peers come in between 1,000 and 1,800 ppm. Thacker Pass, the most advanced project in the country, averages 2,200 ppm. Surge’s deposit runs roughly 50% higher than that.

The geology helps even more. The bulk of Surge’s mineralization sits at or near the surface, with five of the nine 2025 drill holes hitting lithium within 6 meters of surface. The strip ratio is 1.16, well below most clay peers in the 2-to-4 range. That means less waste rock has to move before mining starts, and the highest-grade ore comes out first.

The deposit also remains open in multiple directions. The basin extends to the south and east, with no drill boundary established yet. A 640-meter step-out hole drilled in 2025 returned 4,246 ppm Li from surface, suggesting the resource has room to grow well beyond its current size.

In a category where grade and depth dictate economics, Surge is starting from a stronger position than anyone else in the U.S.

What Thacker Pass Already Proved, Surge Is Now Set Up to Repeat

Thacker Pass is the most important reference point in U.S. lithium right now.

Owned by Lithium Americas (NYSE: LAC), Thacker has attracted more than $3 billion in financing to advance toward production.

The U.S. Department of Energy provided a $2.23 billion loan…General Motors committed $945 million…and Orion Resource Partners added another $250 million. The mine is targeted to begin production in 2028 after a 2027 commissioning period and will become the largest domestic lithium operation in the country.

That matters for Surge for a few reasons.

The first is technical. Thacker uses the same extraction approach Surge plans to use, processing the same type of sedimentary clay deposit, in the same state, with the same regulatory path.

Once Thacker pours first lithium, the entire category gets validated at commercial scale. The technology question that has hung over American lithium development for a decade gets answered.

The second reason is economic. Thacker projects operating costs of $8,039 per tonne of LCE. Surge’s PEA projects $5,243. That means Surge’s projected OPEX is $2,796/t lower than Thacker Pass, representing approximately a 35% cost advantage.

Higher grade means less material moved, less acid used, less energy spent per tonne of finished product. Surge starts with a structural cost advantage that compounds over a 42-year mine life.

The third reason involves capital markets. Thacker began its current cycle as a junior with a sub-$200 million market cap. It now sits north of $4 billion of total project value.

The path between those two points is the same path Surge is walking right now. Same state, same deposit type, same type of process chemistry, with a higher-grade resource and stronger projected economics.

Surge sits roughly five years behind Thacker on the development curve. The blueprint is already drawn.

The Highest Grade Lithium Clay Resource in the United States…Fully Funded and Under Construction

Nevada North is the highest-grade lithium clay resource in the United States — a deposit comparable to Lithium Americas’ Thacker Pass, now fully funded and under construction.

Thacker Pass validated the lithium clay asset class. Nevada North is what comes next.

With superior grades, near-surface mineralization, and a clear path to a construction decision, Surge is advancing Nevada North as rapidly as possible — building on the blueprint Thacker Pass has established, with the advantage of better economics, a stronger resource, and the full benefit of what the industry has learned.

The recently upgraded Mineral Resource Estimate confirms what the geology has always suggested: 87% of the resource has converted to Measured and Indicated, hosting 10.5 Mt LCE at 3,007 ppm Li — including a high-grade core of 6.7 Mt LCE at 3,820 ppm Li — with high grades starting at surface. That is a structural advantage no peer can match.

A $24 Billion Mining Major Already Did the Diligence

In September 2025, Surge signed a joint venture with Evolution Mining (ASX: EVN), one of Australia’s largest gold producers and a global mining company with a market cap above A$24 billion.

Evolution committed up to C$10 million to fund Surge’s Pre-Feasibility Study. Surge retains operatorship and a 70.54% stake in the project. Evolution’s interest grows as it deploys the funding.

Strategic backing from a company of Evolution’s size is massive at this stage of development.

Major mining companies don’t write checks on instinct. Before Evolution committed capital, its technical team conducted months of detailed review covering geology, metallurgy, mine planning, permitting and economics.

That’s the kind of diligence a junior developer can’t replicate on its own, and the kind of validation institutional investors notice when deciding whether to take a position.

The relationship also brings access. Evolution has indicated it will introduce Surge to global banks and institutional investors once the PFS is delivered, potentially as soon as late 2026.

For a junior trading on the TSX Venture Exchange, that kind of introduction can change the shareholder base overnight.

Evolution’s commitment is one of the clearest external signals that Nevada North is being treated as a real project by the mining industry, not just a story.

The Catalysts Stacking Up Between Now and the End of 2026

Surge has more potential near-term catalysts than most lithium developers its size. Here’s what investors should be watching.

Updated Mineral Resource Estimate – Delivered. RESPEC delivered the updated MRE with 10.51 Mt LCE at 3,007 ppm Li in Measured and Indicated categories, converting 87% of the resource — one of the highest conversion ratios in the lithium clay sector — and providing the high-confidence geological foundation for the ongoing Pre-Feasibility Study. Key highlights of the upgrade: grade improves with confidence — M&I grades increased at elevated cutoffs versus the prior Inferred estimate; new M&I resource has been defined outside the original PEA pit, plus 3.1 Mt LCE Inferred extending the footprint further; and Fluor now has the high-confidence foundation to finalize mine design and capital estimates, with PFS delivery targeted Q4 2026.

Salmon River water rights agreement. Surge has been negotiating with the Salmon River Cattlemen’s Association for two years on water rights. An agreement would remove the most cited objection to the project’s water plan and clear a major permitting hurdle. Management has indicated a deal is expected within the next couple of months.

Pre-Feasibility Study delivery. Fluor Corporation, a Fortune 500 engineering firm, was engaged in February 2026 as PFS lead with delivery targeted for Q4 2026. The PFS will refine the project’s NPV and IRR with higher-confidence data and unlock potential eligibility for U.S. government funding programs that require feasibility-stage study completion.

Government funding eligibility. Once the PFS is completed, Surge becomes eligible to apply for the same DOE loan programs Thacker Pass used to secure $2.23 billion in financing.

Each of these is a discrete event that could re-rate the stock on its own. Together, they line up over the next 12 months in a powerful way for Surge Battery Metals.

Why Surge Trades at a Fraction of What the Asset Looks Like It’s Worth

Here’s where it gets interesting for investors looking at Surge today.

The Preliminary Economic Assessment values the project at $9.17 billion in after-tax NPV at $24,000 LCE. The IRR is 22.8%. Surge holds a 70.54% interest. Even applying a heavy discount for early-stage execution risk, the math points to project value well into the billions.

Surge’s current market cap sits below $150 million.

That gap exists for a few reasons. Surge trades on the TSX Venture Exchange, which limits its visibility to U.S. institutional investors. The PFS is not yet complete. And the company is pre-revenue and pre-production. Of course, none of that is unusual for a junior lithium developer.

But the gap also exists because the market hasn’t caught up to what Evolution Mining already saw, what the analysts at SCP Resource Finance, Sprott and Roth already see, and what the comparison to Thacker Pass makes obvious.

History suggests that gap doesn’t last forever. As Thacker advanced through its development milestones, its market cap moved from sub-$200 million to over $4 billion.

Lithium Americas, the operator, now trades at over a billion dollars in its own right. Ioneer (NASDAQ: IONR), with a lower-grade deposit and weaker projected economics than Surge, carries a market cap above US$300 million.

Surge has the higher-grade resource. Surge has the lower projected operating costs. Surge has the major mining partner already funding the next study. Surge has the team that sold its last lithium project for $490 million.

What it doesn’t yet have is the market cap to match. That’s the opportunity.

The Reasons to Look at Surge Today Speak for Themselves

The lithium market has turned. Prices are climbing. Multi-year deficits are now the consensus view across major research desks. Washington is putting billions of dollars behind domestic supply.

In Nevada, one project is positioned better than any other to benefit.

Surge Battery Metals (TSXV: NILI); (OTCQX: NILIF) holds the highest-grade lithium clay deposit in the United States, with a Preliminary Economic Assessment showing $9.17 billion in after-tax NPV, a 22.8% IRR and projected operating costs at $5,243 per tonne. A $24 billion mining major is funding the path to the Pre-Feasibility Study. The team running the company sold their last lithium project for $490 million.

The next 12 months bring a stack of catalysts that could move the story forward in a meaningful way.

And the stock still trades at a fraction of what comparable projects have been valued at on the same development path.

Lithium investors have seen this pattern before. The companies that get noticed early, before the milestones land and the institutions pile in, are the ones that deliver the strongest returns when the cycle plays out.

Surge Battery Metals (TSXV: NILI); (OTCQX: NILIF) is one of those companies right now.

7 Reasons

Why You Should Strongly Consider Surge Battery Metals (TSXV: NILI); (OTCQX: NILIF) Today

1

The Highest-Grade Lithium Clay Deposit in America…Right at the Surface

Grade is the single most important driver of value in any lithium project. And on grade, Surge Battery Metals stands above the U.S. field. The Nevada North Lithium Project hosts 10.51 million tonnes of Lithium Carbonate Equivalent (Measured and Indicated Mineral Resource[iii]). The PEA mine plan grades average 4,016 ppm Li over the 42-year mine life — nearly double the Thacker Pass average of 2,200 ppm. Higher grade means more lithium recovered per tonne of material processed and lower processing costs. The geology offers a second advantage. The bulk of Surge’s resource sits at or near the surface. Thacker’s higher grades are buried deeper, requiring more stripping and blending. Surge can mine its highest-grade ore directly from the surface, which means less waste, lower production costs and stronger margins.

Not All Lithium Deposits Are Equal — Only the Best Get Built.

Across every lithium type — hard rock, brine, DLE, and clay — only the highest-quality, lowest-cost assets will achieve sustained, long-term production. Grade, scale, cost, and deposit continuity determine which projects get built and which ones don’t. The market rewards asset quality, not asset class.

Tier 1 assets — large scale, long mine life, low cost, high margins — get built first and operate through cycles. Nevada North Lithium Project is a clear Tier 1 lithium asset: the highest-grade lithium clay resource in the United States, near-surface and free-dig, with an estimated OPEX of US$5,243/t — delivering a 78% operating margin at $24,000/t LCE — a 42-year mine life, 86,000 tonne per year production scale, and fewer permitting and ESG constraints than peer projects.

NNLP is the leading clay lithium project in North America and is positioned for long-life, low-cost, high-margin production.

2

Following a Proven Blueprint That’s Already Attracted $3 Billion in Capital

The single biggest question facing any new lithium project in North America is whether its extraction method will work at commercial scale. That’s the open question for almost every Direct Lithium Extraction (DLE) project in the country…and none of them have proven the technology at full production yet. The Nevada North Lithium Project, as a clay deposit, doesn’t face that question. Surge’s project uses the same type of process chemistry and the same type of sedimentary clay deposit as Thacker Pass, which has already raised more than $3 billion to advance, including $2.23 billion from the U.S. Department of Energy, $945 million from General Motors and $250 million from Orion. Thacker is targeted to begin production in 2028 after a 2027 commissioning period. When it does, it validates the entire sedimentary clay category. And Surge Battery Metals will be the next major project in line.

3

A $24 Billion Mining Major Is Funding the Next Stage of Development

In September 2025, Evolution Mining (ASX: EVN), a global mining major with a market cap of roughly A$24 billion, signed a joint venture to advance the Nevada North Lithium Project. Evolution committed up to C$10 million to fund Surge’s Pre-Feasibility Study. Surge retains operatorship and a 70.54% stake. Strategic backing of this kind is massive at this stage of development. Major mining companies do extensive technical and financial due diligence before committing capital, and Evolution’s commitment signals that Surge’s Nevada North Lithium Project passed that test. Evolution has also indicated it will help introduce Surge to global banks and institutional investors once the PFS is delivered, which is targeted for Q4 2026. For shareholders, the partnership reduces near-term dilution risk and adds a heavyweight voice to the Surge Battery Metals story.

4

Built to Produce Lithium Cheaper Than Almost Anyone Else

In lithium production, costs are everything. A project that can produce cheaply makes money in any market, while a project that has higher costs gets shut down as soon as prices begin to dip. Surge’s Preliminary Economic Assessment, released in 2025, projects operating costs of just $5,243 per tonne of lithium carbonate equivalent. Thacker Pass, the most advanced lithium clay project in the country, projects operating costs of $8,039 per tonne. That’s a 35% cost advantage for Surge that compounds over a 42-year mine life. The same PEA shows an after-tax NPV of $9.17 billion at $24,000 LCE, a 22.8% IRR and a 4.7-year after-tax payback. Those are the kinds of numbers that get a lithium project built. They’re also the kinds of numbers that are more likely to attract strategic partners and offtake buyers.

5

A 42-Year Mine Plan That Uses Only 30% of the Resource

Most lithium projects have a single mine life and a clear endpoint. Surge’s Nevada North Lithium Project is built on a different scale entirely. The PEA outlines a 42-year mine plan that processes only 30% of the current resource. The remaining 70% offers decades of additional production potential beyond the initial mine life. This makes Nevada North a true multi-generational asset. And it also gives Surge room to scale production over time as demand grows, without ever running short on feed material. A 10.51-million-tonne LCE resource (Measured and Indicated Mineral Resource[iv]) with decades of upside beyond the mine plan puts Surge in rare company.

6

The Same Team That Sold Millennial Lithium for $490 Million

In lithium development, plenty of projects look good on paper…but far fewer ever get built. Surge’s team has successfully done this before. Chairman Graham Harris founded Millennial Lithium and sold it to Lithium Americas for US$490 million in 2022. He brought core members of that team with him to Surge, including Director Iain Scarr – who brings over 30 years of experience from Rio Tinto – and metallurgy expert Dr. Vijay Mehta, who brings over 50 years of industry experience and specializes in the technological and economic feasibility of battery-grade lithium brine processing. Surge has also added Steffen Ball, formerly of Nissan North America and Ford Motor Company, to drive OEM and offtake conversations. And Richard Weech, who led Berkshire Hathaway Energy’s renewables and lithium investments from 2014 to 2022, joined the board in early 2026 as an independent director. Resumes like these don’t show up at junior lithium companies by accident.

7

Made-in-America Lithium, Right When Washington Wants It Most

The United States imports more than 95% of its lithium, primarily from China and Chinese-controlled operations in South America and Africa. That kind of dependency is no longer politically acceptable. Washington is now putting billions of dollars behind projects capable of producing critical minerals on American soil. Thacker Pass alone secured a $2.23 billion loan from the U.S. Department of Energy. Surge’s Nevada North Lithium Project sits in the heart of this push, in the most established mining jurisdiction in North America, with infrastructure, a skilled workforce and a regulatory framework built for resource development. Surge is not yet eligible for federal financing because it remains pre-PFS…but as the company advances toward feasibility, it may become eligible for the same kind of project-boosting government support Thacker received.

-

Sienna Resources Engages Terraquest Ltd. for Saskatchewan Airbourne Survey...

06/16/2026 07:01 AMVancouver, British Columbia--(Newsfile Corp. - June 16, 2026) - Sienna Resources Inc. (TSXV: SIEN) (OTCID: SNNAF) (WKN: A418KR) (the "Company" or "Sienna") wish...

-

Surge Battery Metals Announces Strategic Funding to Fast Track the Nevada North ...

06/03/2026 02:00 PMBrian Paes-Braga - Managing Partner at SAF Group, Founder of Lithium X - and Michael Hess, CIO of Hess Capital, Co-Chairman of The Metals Royalty Company, and B...

-

RK Equity Initiates Research Coverage on Surge Battery Metals...

06/01/2026 01:30 PMWest Vancouver, British Columbia--(Newsfile Corp. - June 1, 2026) - Surge Battery Metals Inc. (TSXV: NILI) (OTCQX: NILIF) (FSE: DJ5) (the "Company" or "Surge") ...

-

Surge Battery Metals Reports Optimization of Flowsheet Parameters and Extraction...

05/26/2026 12:00 PMWest Vancouver, British Columbia--(Newsfile Corp. - May 26, 2026) - Surge Battery Metals Inc. (TSXV: NILI) (OTCQX: NILIF) (FSE: DJ5) (the "Company" or "Surge") ...

-

CEO.CA's Inside the Boardroom: Surge Battery Metals Further De-Risks Highest-Gra...

05/19/2026 10:34 PMToronto, Ontario--(Newsfile Corp. - May 19, 2026) - CEO.CA ("CEO.CA"), the leading investor social network in junior resource and venture stocks, shares exclusi...

-

Surge Announces Resource Upgrade at Nevada North: 657.5 Mt Grading @ 3,007 ppm L...

05/14/2026 11:00 AMWest Vancouver, British Columbia--(Newsfile Corp. - May 14, 2026) - Surge Battery Metals Inc. (TSXV: NILI) (OTCQX: NILIF) (FSE: DJ5) (the "Company" or "Surge") ...

-

Surge Battery Metals Announces Application to List on NASDAQ Capital Markets...

05/06/2026 12:00 PMWest Vancouver, British Columbia--(Newsfile Corp. - May 6, 2026) - Surge Battery Metals Inc. (TSXV: NILI) (OTCQX: NILIF) (FSE: DJ5) (the "Company" or "Surge") i...

-

Surge Battery Metals Inc. Announces Investor Relations and Marketing Agreements...

05/01/2026 12:00 PMWest Vancouver, British Columbia--(Newsfile Corp. - May 1, 2026) - Surge Battery Metals Inc. (TSXV: NILI) (OTCQX: NILIF) (FSE: DJ5) (the "Company" or "Surge") a...

-

ExGen Signs Purchase Agreement to Acquire Lithium Properties in Nevada...

04/30/2026 09:00 PMNOT FOR DISTRIBUTION TO UNITED STATES NEWSWIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES VANCOUVER, British Columbia, April 30, 2026 (GLOBE NEWSWIRE) -...

[i] https://www.technologyreview.com/2026/01/22/1131563/lithium-2026/

[ii] Mineral resources are not mineral reserves and do not have demonstrated economic viability.

[iii] Mineral resources are not mineral reserves and do not have demonstrated economic viability.

[iv] Mineral resources are not mineral reserves and do not have demonstrated economic viability.

[v] https://www.capitalbrief.com/briefing/lithium-miners-soar-as-ubs-lifts-forecast-prices-180e1e51-1bd2-4dad-a702-78808d496269/

[vi] https://ca.investing.com/news/analyst-ratings/scotiabank-upgrades-lithium-argentina-stock-on-multiyear-lithium-rally-forecast-93CH-4396999

[vii] https://www.metals-hub.com/en/blog/whats-driving-lithium-demand-in-2025-and-beyond/

[viii] https://www.usgs.gov/news/national-news-release/lithium-eastern-states-could-replace-imports-a-century-or-more

[ix] https://www.usgs.gov/news/national-news-release/lithium-eastern-states-could-replace-imports-a-century-or-more

[x] Mineral resources are not mineral reserves and do not have demonstrated economic viability.

FULL DISCLAIMER

This website and newsletter are owned, operated, and edited by Jade Cabbage Media LLC (“Jade Cabbage,” “we,” “us,” or “our”). Any reference to “I,” “we,” “our,” or “Jade Cabbage” refers exclusively to Jade Cabbage Media LLC.

This communication is a paid advertisement. It is not a recommendation to buy or sell any security, nor is it investment advice. Jade Cabbage Media LLC is not registered as an investment adviser, broker-dealer, or in any other capacity with the U.S. Securities and Exchange Commission or any state securities regulator. We are not qualified to provide investment recommendations.

By accessing or reading our website or newsletter, you agree to the terms of this Disclaimer, which we may update at any time without notice. Your continued use constitutes acceptance of the current version.

We are compensated to create awareness for publicly traded companies.

Our business model is based on receiving financial compensation for marketing and investor relations services. You should therefore assume we have an inherent conflict of interest and may not be unbiased.

Specific Campaign Disclosure – Surge Battery Metals Inc (NILI) Pursuant to an agreement with Winning Media LLC, Jade Cabbage Media LLC has been engaged (indirectly through Winning Media LLC) to assist with investor awareness and marketing activities for Surge Battery Metals Inc (NILI).

The campaign period is May 4, 2026 through July 3, 2026.

Winning Media LLC received $200,000 via bank wire for these services.

We expect to receive additional compensation as the awareness campaign continues and will disclose all amounts received.

As of the date of this communication, Jade Cabbage Media LLC and its principals own zero shares of Surge Battery Metals Inc (NILI). We may sell any shares we acquire at any time without notice, which could negatively affect the stock price.

This compensation creates a significant conflict of interest.

Therefore, this entire communication must be viewed solely as a commercial advertisement.

Important Warnings

We do not provide investment advice. Never make investment decisions based on our content.

Always conduct your own thorough due diligence and consult with a licensed financial advisor or investment professional before investing.

Micro-cap and low-priced securities are highly speculative and carry a high risk of loss. Only invest capital you can afford to lose entirely.

Past performance or mentioned price gains are not indicative of future results. Gains referenced may be based on intraday or end-of-day prices.

Companies we profile may experience increased volume and price during marketing campaigns, which often decline once the campaign ends.

The hiring party or its affiliates may sell shares of the profiled company at or near the time you receive this communication, which could negatively impact the stock price.

We have not independently investigated the background or operations of any profiled company.

No Guarantees All information is obtained from publicly available sources (company websites, press releases, etc.) and has not been independently verified by us. We do not guarantee the accuracy, completeness, or timeliness of any information. Independent contractor writers are sometimes used; although their work is reviewed, errors or omissions may still occur.

Forward-looking statements are subject to risks and uncertainties and are not guarantees of future performance.

Limitation of Liability To the fullest extent permitted by law, you agree that Jade Cabbage Media LLC, its owners, officers, employees, contractors, affiliates, and successors shall not be liable for any direct, indirect, incidental, consequential, or punitive damages (including loss of profits or investment losses) arising from your use of our website, newsletter, or any information contained therein. You assume all risks associated with any investment decisions you make.

Entertainment & Educational Purposes Only Our content is provided for entertainment and general information purposes only and should never be the sole basis for any investment decision.

You are strongly encouraged to review all publicly available information on the profiled companies at the U.S. Securities and Exchange Commission’s website: www.sec.gov.