Sponsored – Est. Read 7 Min

One of Argentina’s Last High-Grade Lithium Brine Projects… Still Trading at a Fraction of its Peer Valuations

NOA Lithium Brines (TSXV: NOAL);(OTCPK: NLIBF) controls a 4.7 million tonne lithium resource with a PEA pointing to billions in value…but it still trades at just roughly C$70 million.

The window on a unique, high-grade lithium opportunity in Argentina is closing fast.

Most of the best salars were claimed long ago or locked up under long-term offtakes.

What’s left in the world’s most prolific lithium-producing district is mostly either lower-grade, earlier-stage, or already spoken for.

Some would say there are no new opportunities worth considering in this historic region.

But those who would say that are dead wrong…

And that’s precisely why NOA Lithium Brines (TSXV: NOAL); (FSE: N7N); (OTCPK: NLIBF) deserves a closer look right now.

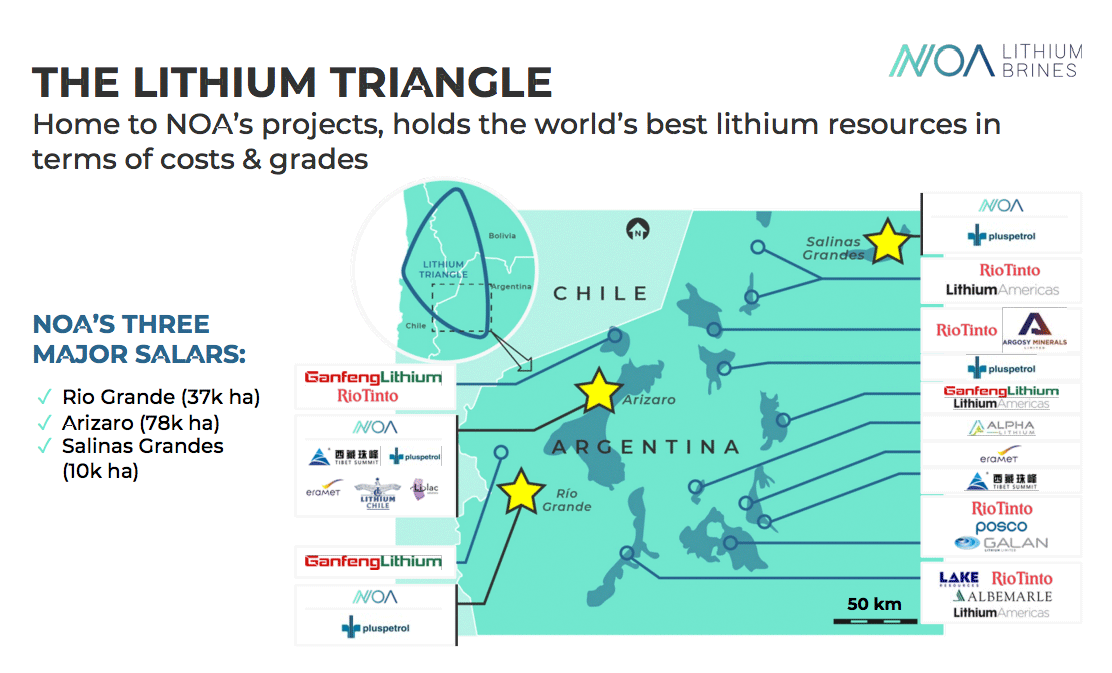

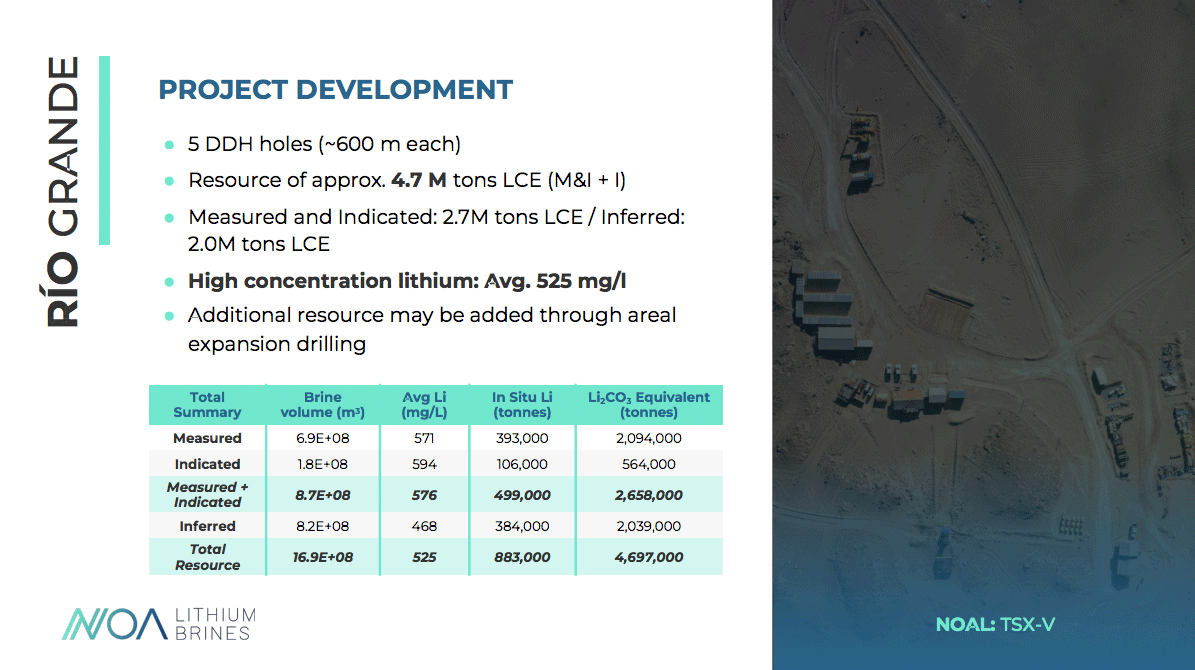

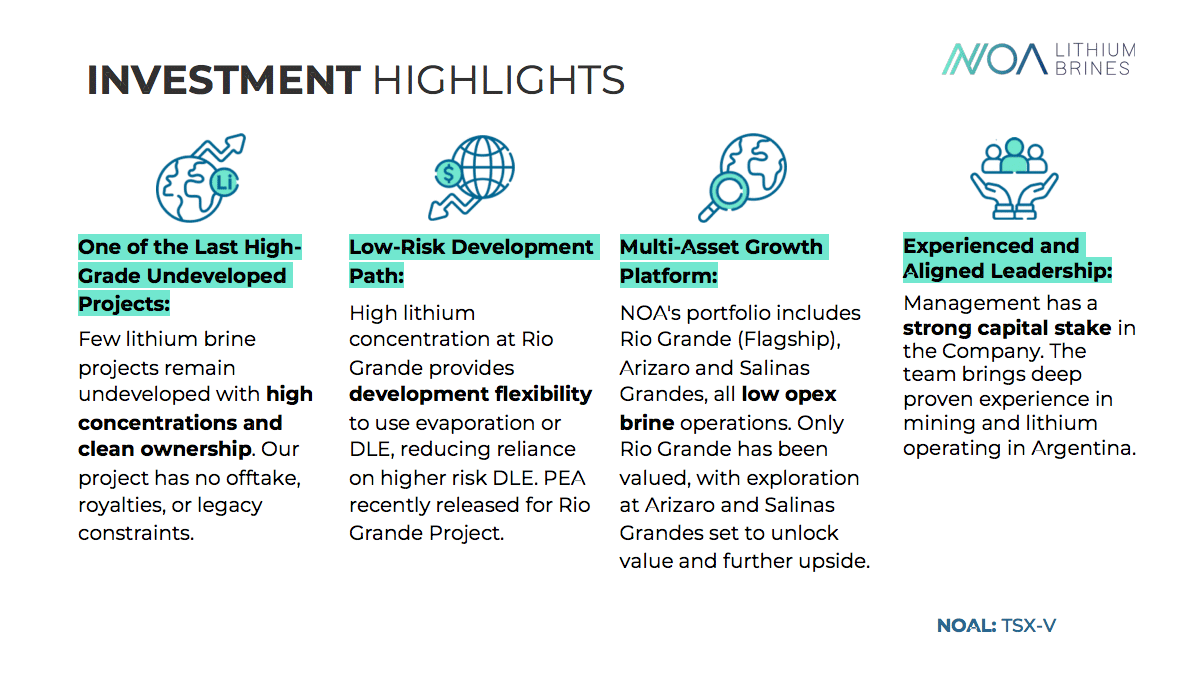

The company’s flagship Rio Grande project hosts 4.7 million tonnes of lithium carbonate equivalent at average grade above 500 mg/L, making it one of the highest-concentration brine resources still to be developed in the region.

Very few lithium brine projects in this region remain undeveloped with high concentrations and clean ownership.

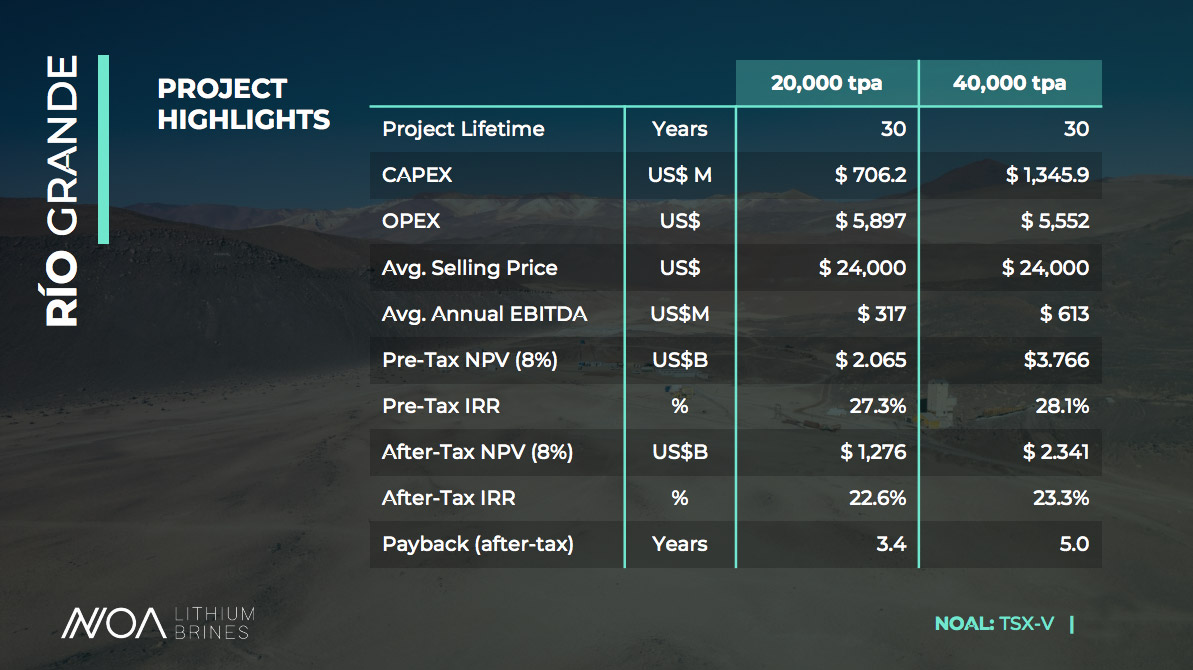

A completed PEA already outlines project economics at Rio Grande that could be worth over $2 billion for a single train of 20,000 tonnes production or as much as $3.8 billion at full capacity of 40,000 tonnes per year. And the project has no offtakes, royalties or legacy constraints.

In other words, NOA Lithium Brines offers investors access to one of the last high-grade undeveloped projects in the famous Lithium Triangle.

And yet, despite all of that, NOA Lithium Brines currently trades at a valuation of around just C$70 million.

The math doesn’t add up…and that’s the opportunity.

Comparable lithium brine developers in Argentina have commanded valuations three to four times higher, often with lower grades and smaller resources.

Meanwhile, lithium prices have already more than doubled off their mid-2025 lows and Australian lithium equities have run four- and five-fold on the recovery.

Here in North America, most lithium stocks haven’t moved on this price rebound yet…making the opportunity with NOA Lithium Brines even more attractive today.

NOA Lithium Brines offers a high-grade, PEA-stage asset with multi-billion-dollar economics in the world’s most prolific lithium-producing district…and it’s trading like the market hasn’t noticed.

Here’s why that could change.

7 Critical Reasons

Why You Should Consider NOA Lithium Brines (TSXV: NOAL); (FSE: N7N); (OTCPK: NLIBF) Today

1

One of the Last High-Grade Lithium Brine Assets of Scale

Most of Argentina’s best lithium salars are already spoken for. What remains is mostly lower-grade, earlier-stage, or locked up under offtakes and royalties. Rio Grande is the exception with 4.7 million tonnes of lithium carbonate equivalent at an average of 525 mg/L, among the highest-grade brine concentrations in Argentina’s area of the Lithium Triangle. That combination of scale and grade is nearly impossible to find today without buying into someone else’s deal. NOA Lithium Brines owns it outright, with no legacy constraints attached.

2

A PEA That Already Points to Billion-Dollar Project Value

Rio Grande is unique because it’s a well-defined asset with impressive economics already on paper. The completed Preliminary Economic Assessment (PEA) outlines a two-stage development with 20,000 tonnes per year initially…before scaling to 40,000 tonnes. At full buildout, the project’s pre-tax net present value approaches $4 billion. Even a single-stage operation points to NPV north of $2 billion. And keep in mind: this is the math on an asset that’s currently trading at a C$70 million market cap. The market is pricing NOA like the PEA doesn’t exist.

3

Peer Valuations Expose a Clear Disconnect

Lithium Chile controls a lower-grade brine resource of around 4 million tonnes in Argentina’s Lithium Triangle. It’s a smaller resource than NOA Lithium Brines’ Rio Grande project…and with lower concentrations that limit its development to Direct Lithium Extraction (DLE) technologies only, with no possibility to use commercially proven evaporation process like the case of NOA Lithium. Yet that company is reportedly under acquisition discussions valuing an 80% stake at $175 million USD. Do the math: that’s three to four times NOA Lithium Brine’s entire market cap, for an inferior asset. NOA Lithium Brines has higher grades, a larger resource, and a completed PEA with billion-dollar economics. Yet it still trades at a fraction of what the market is willing to pay for less. Gaps like this don’t stay open forever.

4

Brine Economics That Work Even When Prices Pull Back

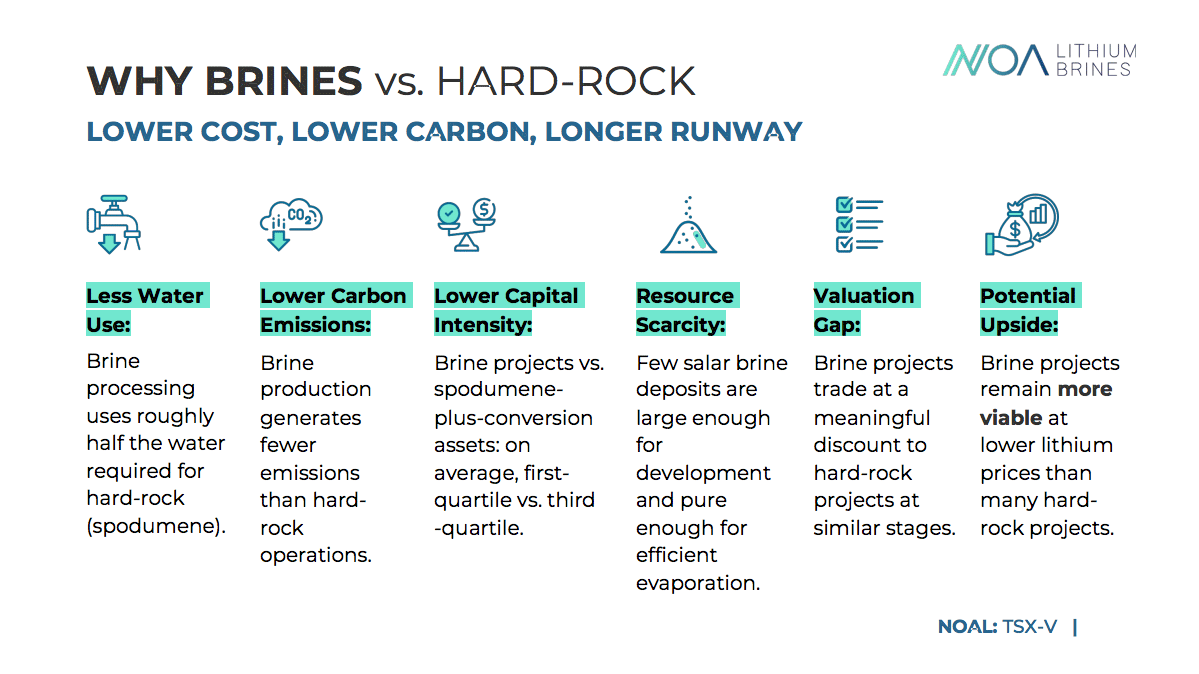

Lithium markets are cyclical. Not every project survives a downturn. That’s where brine assets have a structural edge over hard rock operations thanks to lower capital intensity, lower operating costs and better margins across the cycle. But the advantage goes deeper than cost. Brine projects produce lithium carbonate directly. Hard rock mines in Australia and Africa produce an intermediate concentrate that has to be shipped to China for refining. NOA Lithium Brines’ Rio Grande project doesn’t need elevated prices or a refinery in order to work. That’s the kind of resilience that attracts partners when the market gets selective.

5

Clean Ownership Creates Strategic Flexibility

One of the most underappreciated advantages of NOA Lithium Brines’ Rio Grande project is what it doesn’t have: no legacy offtake agreements, no royalties, no partners or co-owners in any of its projects and no structural constraints that limit the company’s strategic options. That’s rare in Argentina’s lithium sector, where most quality assets already have strings attached. For NOA Lithium Brines, it means full flexibility…no matter if that’s choosing the right development partner, negotiating financing on favorable terms, or positioning for an outright sale. When a major comes looking for high-grade brine exposure, NOA can say yes on its own terms.

6

A Management Team That’s Successfully Done This Before

CEO Gabriel Rubacha has been developing lithium projects in Argentina since the country’s first operation came online in 1997. He was CEO of Minera Exar and President of South American Operations for Lithium Americas. NOA Lithium Brines has a proven leadership team in place with 30 years of experience navigating the exact regulatory, technical, and operational challenges the company will face. Management owns roughly 12% of NOA, which means their incentives are aligned with shareholders and with the rest of the founding group control approximately 22%. Management has been providing funding to the company during difficult periods and has recently exercised additional warrants. When insiders have that much skin in the game, it says something important about the upside potential for the company.

7

Two Additional Salar Assets the Market Isn’t Valuing

Rio Grande is the flagship for NOA Lithium Brines, but it’s not the whole story. NOA also holds 78,000 hectares in the Arizaro salar, representing one of the largest land positions in that salar and an additional 10,000 hectares in the Salinas Grandes salar, with strong infrastructure access. The market is valuing NOA as if only Rio Grande exists. These two projects are essentially free “add-ons”. As Rio Grande advances and attracts attention, Arizaro and Salinas Grandes give NOA additional ways to create value, whether through drilling, partnerships, or spin-off transactions. You’re buying the flagship and getting two district-scale assets thrown in as a bonus.

Sprott: Lithium Enters a New Era of Strategic Demand and Policy Support

The Lithium Market Has Already Turned… But Most North American Stocks Haven’t Caught Up Yet

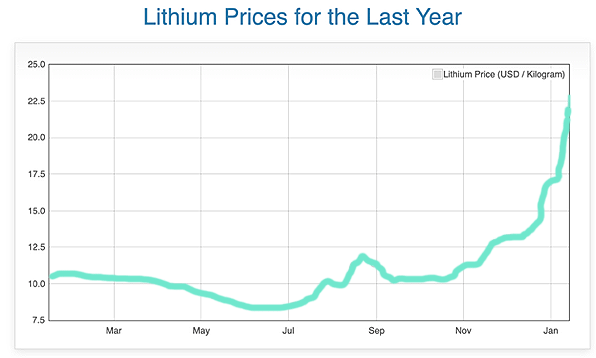

If you followed lithium in 2023 and early 2024, you watched one of the sharpest commodity corrections in recent memory. Prices fell from historic highs above $80,000 per tonne to under $8,000. Marginal projects got shelved. Explorers went quiet. The market moved on.

But here’s what happened next…and what most investors missed.

Lithium prices have already rebounded significantly off those lows. Spot prices have climbed back above $20,000 per tonne and the trajectory is pointing higher.

The reasons aren’t hard to find:

EV adoption continues to accelerate globally…

demand for Battery Energy Storage Systems (BESS) is growing faster than anticipated thereby becoming a new driver of lithium prices…

battery manufacturing capacity is expanding faster than new lithium supply can come online…

…and several high-profile mine delays have tightened the market faster than expected.

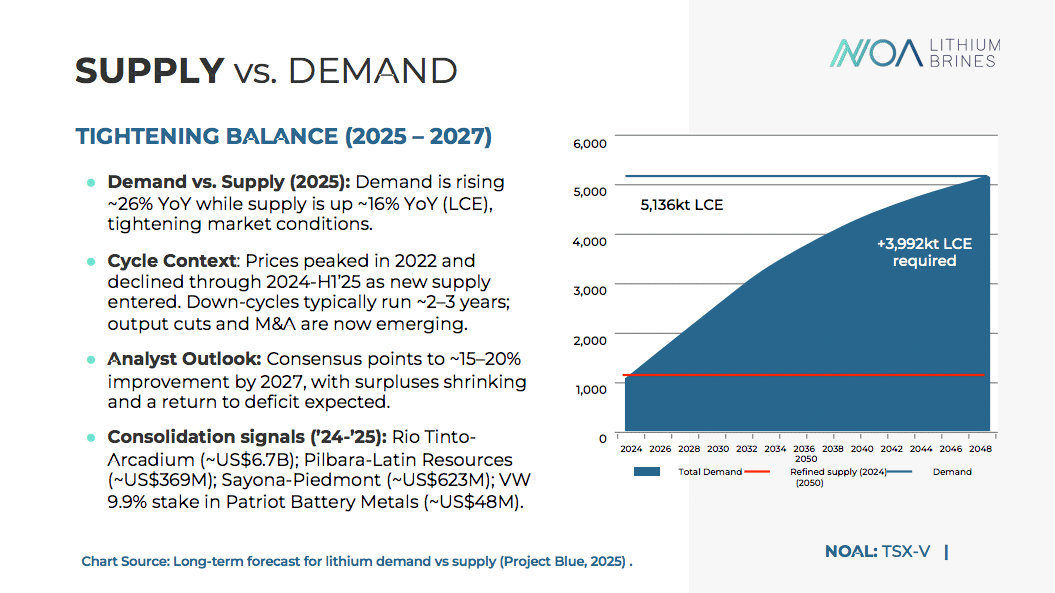

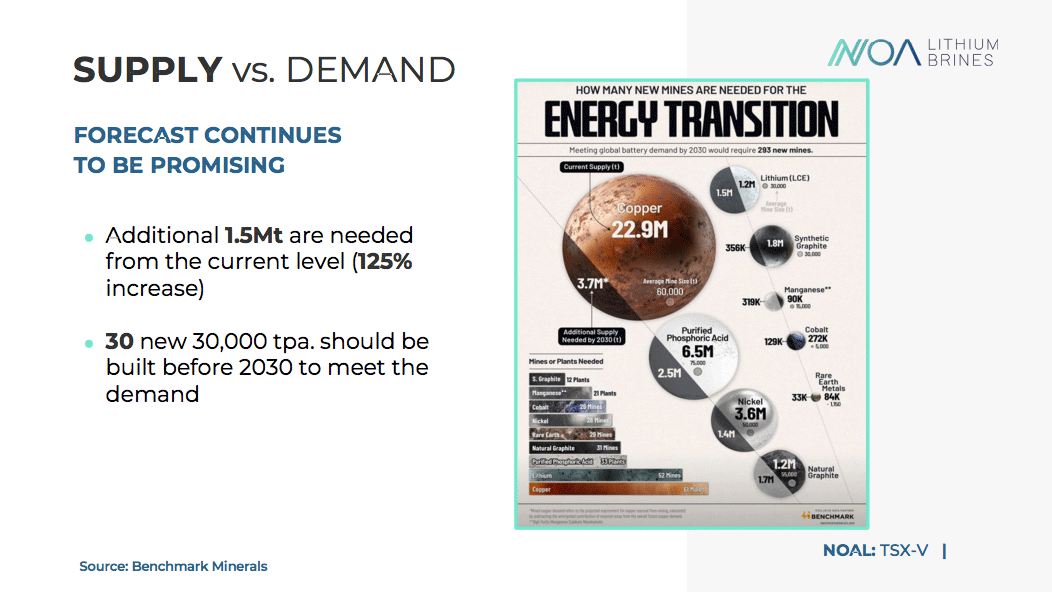

The supply-demand math hasn’t changed. If anything, it’s gotten more compelling. Analysts still project structural deficits by the end of the decade as demand from EVs, grid storage, and consumer electronics outpaces new production, and many are revising their forecasts to anticipate that the deficit could emerge earlier, potentially as soon as this year or 2027.

The projects that will fill that gap need to be moving through development now, which is exactly where NOA Lithium Brines sits.

What’s remarkable is how unevenly the recovery has played out across markets.

In Australia, lithium equities have already re-rated dramatically. Names that were left for dead 18 months ago have run four- and five-fold on the price rebound during the last 6 months. Investors there recognized the turn early and moved aggressively.

Here in North America, that hasn’t happened yet. Many lithium stocks on Canadian and U.S. exchanges are still trading near their lows, as if the commodity recovery never occurred.

For investors paying attention, that gap represents an opportunity. The commodity has moved. The fundamentals support further strength. And an entire segment of the market, including high-quality developers like NOA Lithium Brines, is being priced as if none of it matters.

When North American lithium stocks catch up to the commodity, the re-ratings could be significant. And NOA Lithium Brines offers exactly the kind of asset that benefits most from a market wake-up: high-grade, PEA-stage, with billion-dollar economics and a valuation that still reflects the bottom of the cycle.

4.7 Million Tonnes of High-Grade Lithium…A PEA Pointing to Billions in Value…And a Market Cap of Just C$70 Million: NOA Lithium Brines’ (TSXV: NOAL); (FSE: N7N); (OTCPK: NLIBF) Rio Grande Project

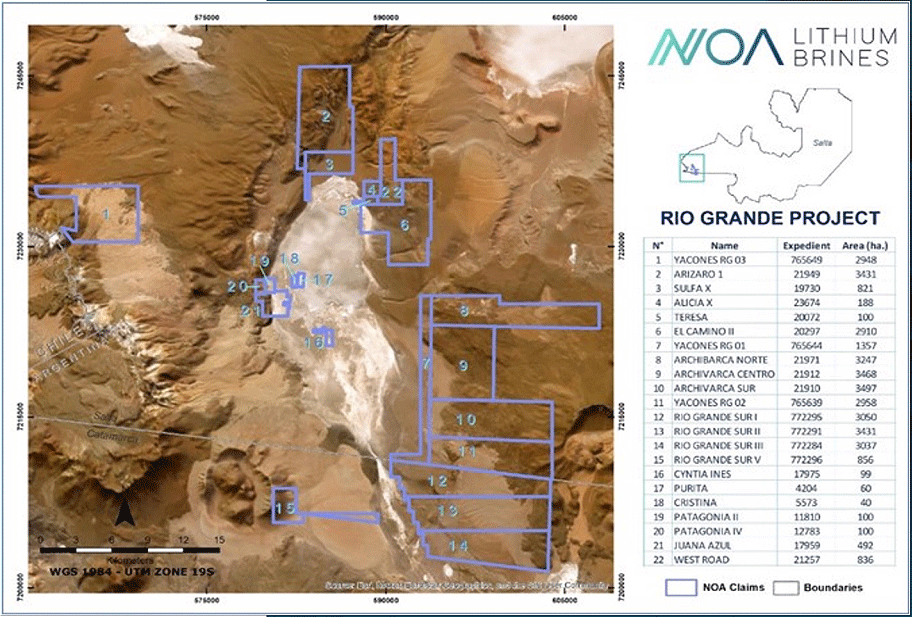

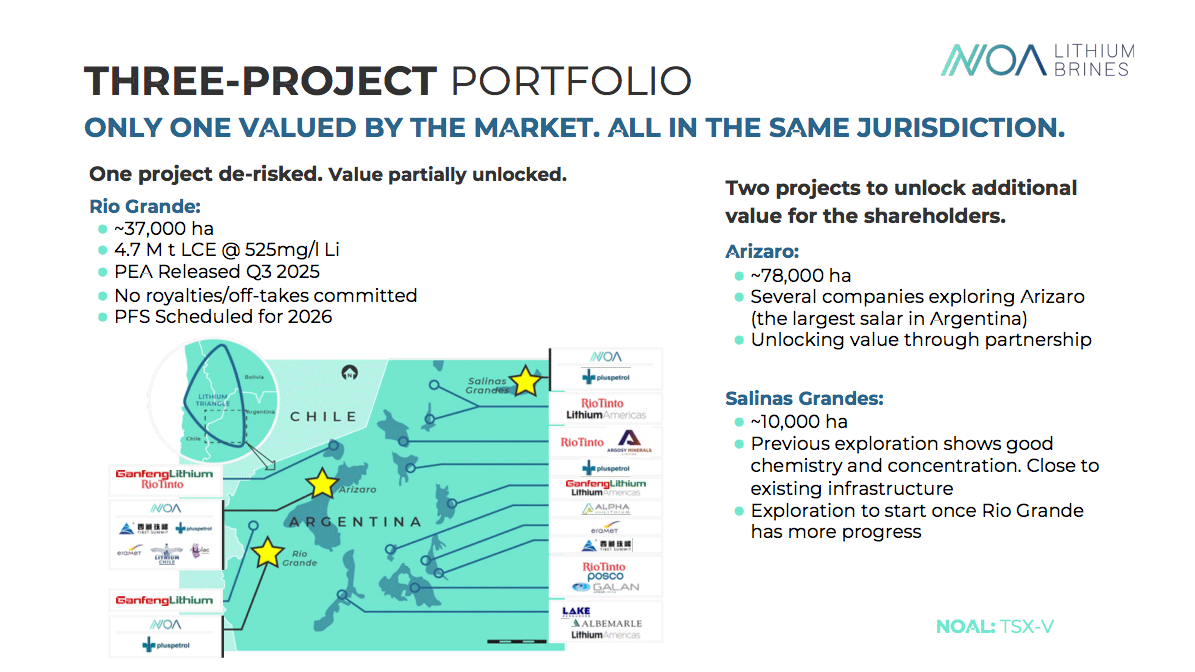

NOA Lithium Brines controls a 100% interest in approximately 37,000 hectares of claims located at the Rio Grande Salar in Salta Province, Argentina.

Situated in Argentina’s Salta Province, which is in the heart of the Lithium Triangle, the project hosts 4.7 million tonnes of lithium carbonate equivalent at 525 mg/L.

That concentration makes it one of the highest-grade brine resources still available in the entire region, and high grades translate directly into better economics.

Keep in mind, the impressive numbers for the Rio Grande project aren’t promotional estimates. They come from a fully documented resource report following NI 43-101 standards, which is the same disclosure framework required of every mining company listed on a Canadian exchange.

The project has a 4.7 million tonne LCE, with approximately 60% classified as measured and indicated resources, the categories that carry the most confidence.

Now let’s put the scale of this project in context: The Rio Grande project alone holds enough lithium to supply a mid-sized battery factory for decades.

Impressive Economics For a Project At This Stage

Most early-stage lithium companies are still drilling holes and hoping the numbers work out. NOA Lithium Brines has moved well past that point with the Rio Grande project.

The completed Preliminary Economic Assessment outlines a two-stage development plan:

Stage one: 20,000 tonnes per year of lithium carbonate production.

Stage two: Expansion to 40,000 tonnes per year.

At full buildout, the PEA projects a net present value approaching $4 billion for the Rio Grande project. Even the first stage alone points to NPV north of $2 billion.

These aren’t aspirational targets. These numbers are the output of engineering work that has been carefully developed and reviewed by independent technical consultants.

No Chinese Refinery Required: Why Brine Beats Hard Rock

Not all lithium is created equal.

Hard rock lithium operations, like the kind you find in Australia, mine spodumene ore.

That ore has to be processed into a concentrate, then shipped overseas (usually to China) for further refining before it becomes battery-grade material. It’s a long supply chain with multiple cost centers and dependencies.

Not to mention the risks that are involved.

Brine operations work very differently.

At Rio Grande, lithium-rich water is pumped from underground aquifers into evaporation ponds…and the sun does most of the work.

What comes out the other end is battery-grade lithium carbonate…ready for cathode manufacturing without a refinery in the middle.

That matters for two important reasons.

First, operating costs are structurally lower because you’re not paying to crush, ship, and refine an intermediate product. Second, you’re not dependent on external processing capacity that may or may not be available when you need it.

High Grades Mean Low-Risk, Proven Processing at Rio Grande

Here’s something that often gets overlooked: Rio Grande’s high lithium concentration means NOA Lithium Brines can use commercially proven evaporation technology rather than experimental direct lithium extraction (DLE) methods.

DLE has generated a lot of headlines. The technology promises to extract lithium faster and from lower-grade brines. But it’s still largely unproven at commercial scale, and the capital costs are significantly higher.

Rio Grande’s grade doesn’t require DLE, providing flexibility for the project development. The grades are high enough that conventional evaporation works…and the technology has been operating successfully in South America for decades.

The Kind of “No Strings Attached” Ownership Structure Acquirers Look For

Most quality lithium assets in Argentina already have commitments attached. This can include offtake agreements that lock up future production, royalty obligations that cut into margins or legacy ownership structures that complicate decision-making.

NOA’s Rio Grande project has none of that.

No offtakes. No royalties. No joint venture partners with blocking rights.

That clean ownership profile gives NOA Lithium Brines something increasingly rare in this sector: optionality.

When the time comes to bring in a development partner, negotiate project financing, or consider a strategic transaction, NOA can evaluate opportunities on their merits…not work around constraints inherited from earlier deals.

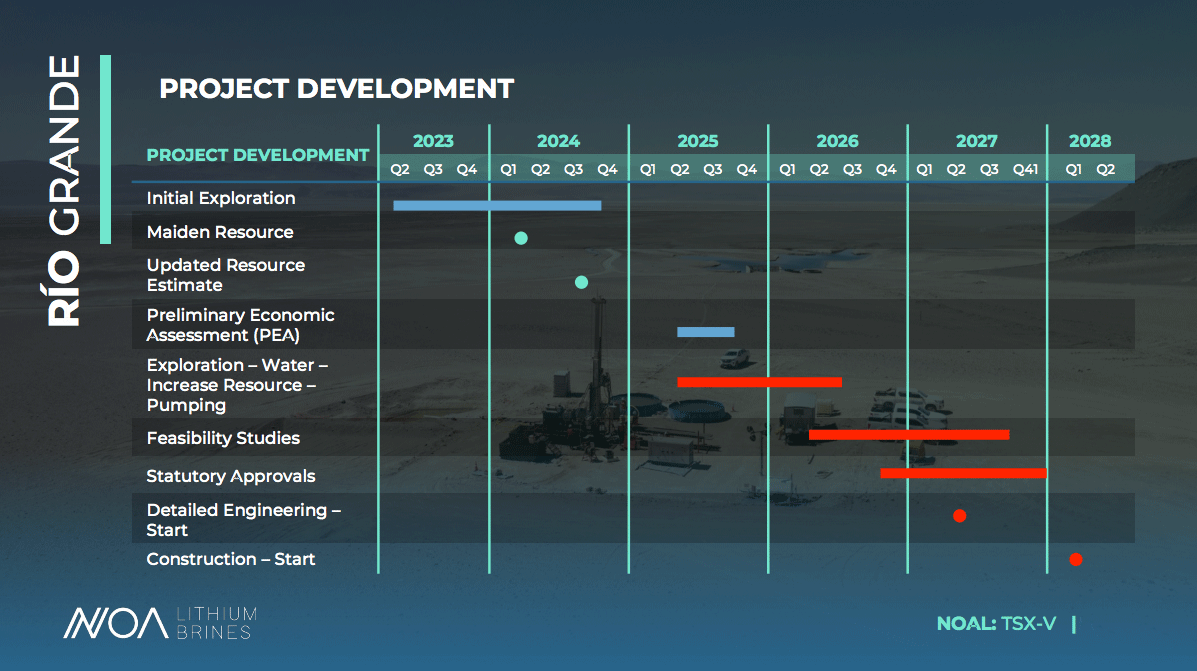

What’s Next for NOA Lithium Brines’ Rio Grande Project

NOA is targeting to complete Rio Grande’s Pre-Feasibility Study before year-end 2026. That’s a significant de-risking milestone.

The PFS will add another layer of technical and economic detail to the project, including more refined capital cost estimates, updated resource models, and more detailed engineering work. For investors, it’s the next validation point that moves Rio Grande closer to development-ready status, and a potential higher valuation for the Rio Grande project and NOA Lithium.

The production target is 2030.

Between now and then, the catalysts to watch are PFS completion, potential strategic partnerships, and broader market recognition of the valuation gap we’ve outlined.

Each milestone brings Rio Grande closer to the kind of project that attracts serious development capital…and narrows the disconnect between what this asset is worth on paper and what the market is currently paying for it.

Beyond the Flagship Asset: NOA Lithium Brines Also Controls Two District-Scale Assets the Market Isn’t Pricing

Rio Grande is the centerpiece of the NOA Lithium Brines story. But it’s not the whole story.

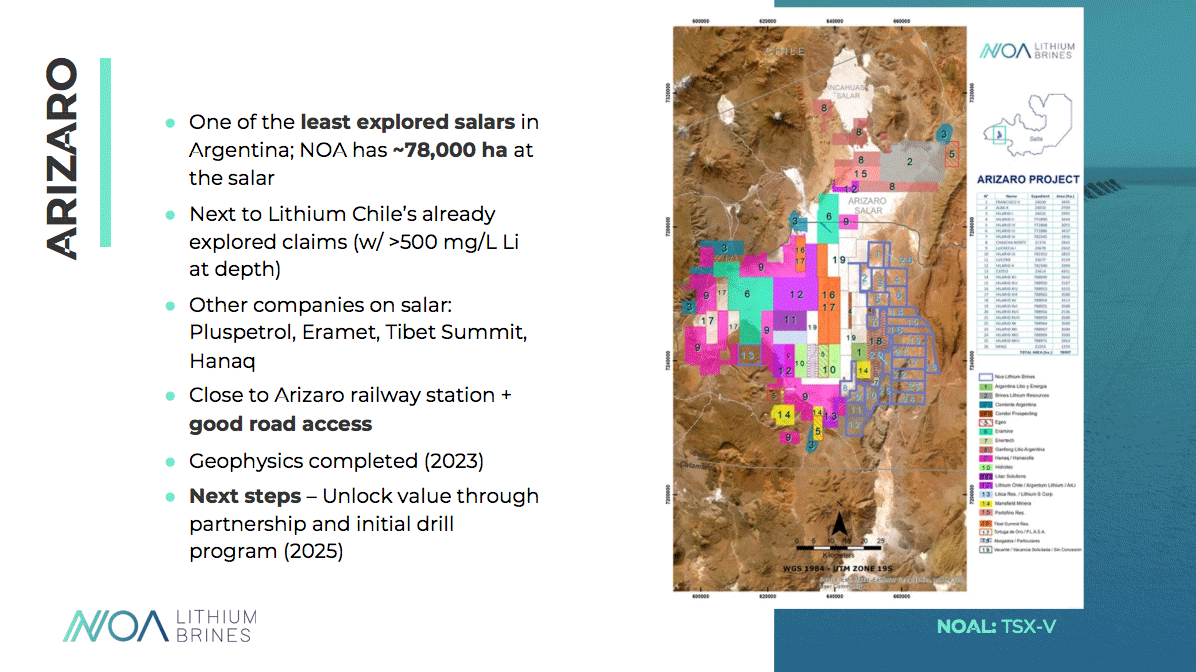

NOA also controls two additional salar projects, Arizaro and Salinas Grandes, that together represent nearly 90,000 hectares of additional lithium-prospective ground in Argentina’s most prolific producing region.

The market is valuing NOA as if these assets don’t exist. That’s a mistake.

Arizaro: Scale That’s Hard to Ignore

At 78,000 hectares, Arizaro is one of the largest land positions in the Arizaro Salar, the largest salar in Argentina’s lithium sector. The project sits in the same geological neighborhood as Rio Grande, within the proven brine-hosting formations that have already been explored by several companies, including Lithium Chile, whose flagship project is located in that salar .

Size alone doesn’t make a project, but it does create optionality. A land position this large offers multiple target areas for future exploration…and multiple ways to unlock value.

NOA Lithium Brines is currently seeking a partnership for the Arizaro project. A potential deal could bring in capital to advance the project while validating the strategic value of the asset, thereby unlocking value without losing focus on Rio Grande.

For NOA shareholders, it would mean exposure to Arizaro’s upside without bearing the full cost of exploration.

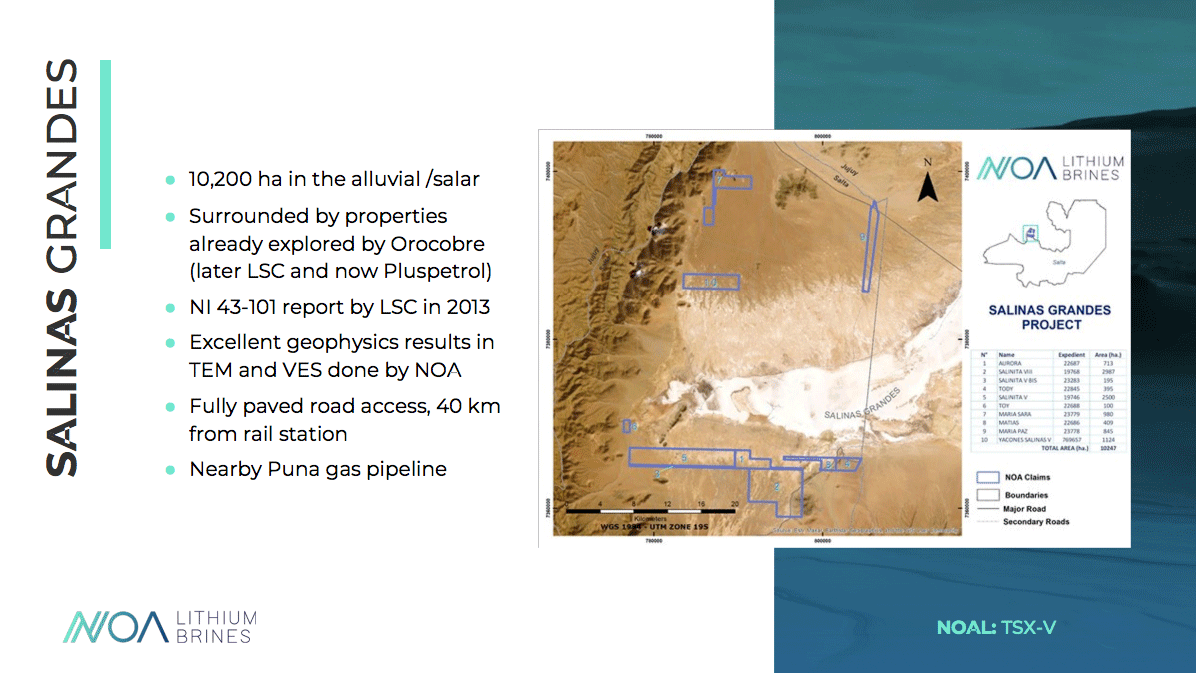

Salinas Grandes: Infrastructure and Accessibility

Salinas Grandes covers approximately 10,000 hectares with one key advantage that often gets overlooked in early-stage projects: infrastructure access.

Roads, power, and logistics matter when it comes time to develop a lithium project. Salinas Grandes benefits from proximity to existing infrastructure, which could translate into lower development costs and a faster path to production if the resource proves out.

NOA has drilling planned for Salinas Grandes in 2026.

That program will test the lithium potential of the salar and could add resource upside that isn’t currently reflected in the company’s valuation.

The Bonus You’re Not Paying For

Here’s the way to think about the opportunity with NOA:

At today’s market cap, you’re buying NOA Lithium Brines for Rio Grande. The 4.7 million tonne resource. The PEA with billion-dollar economics. The high-grade concentration and clean ownership.

Arizaro and Salinas Grandes essentially come along for free.

If either project delivers – either through drilling success, a partnership deal, or eventual development – that’s upside shareholders aren’t paying for today.

If neither pans out, you still own one of the last high-grade undeveloped brine assets in Argentina’s Lithium Triangle.

That’s the kind of risk-reward asymmetry that rarely lasts.

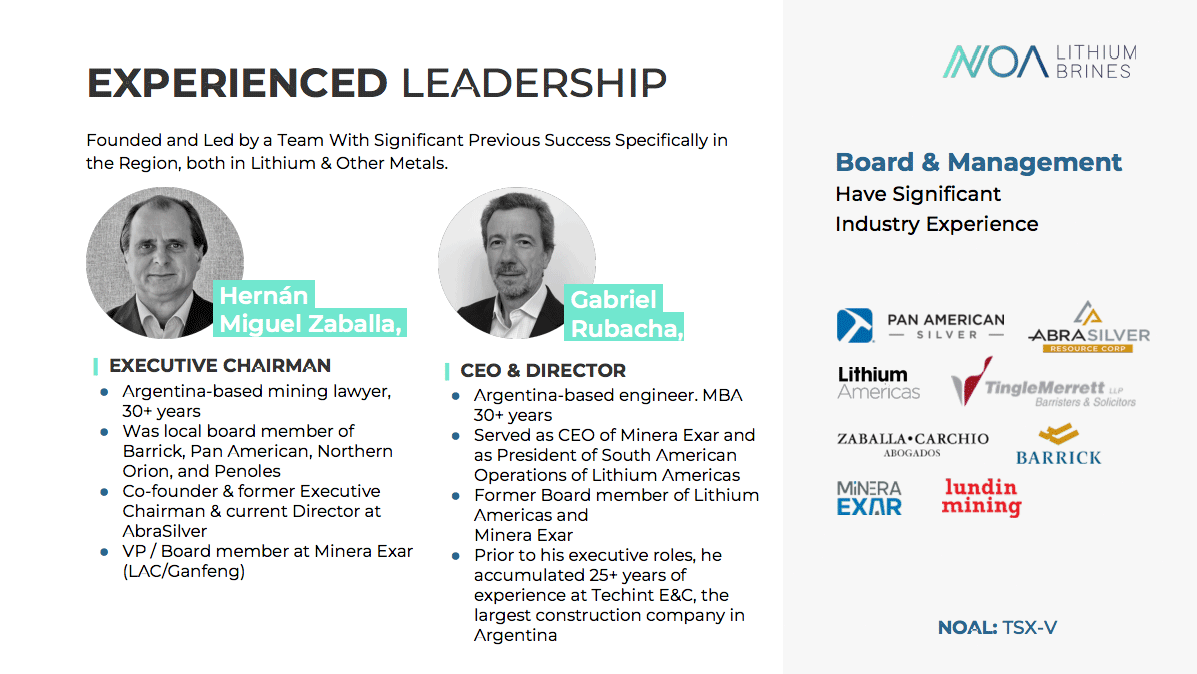

A Proven, Successful Team Leading the Way For NOA Lithium Brines

A great asset means nothing without the right people to develop it. NOA Lithium Brines has that covered.

CEO Gabriel Rubacha has been building lithium projects in Argentina since the country’s first operation came online in 1997. That’s nearly three decades of direct, on-the-ground experience in the exact region where Rio Grande sits.

His track record speaks for itself. Gabriel served as CEO of Minera Exar and President of South American Operations for Lithium Americas, two of the most significant lithium development stories to come out of Argentina.

Mr. Rubacha together with Executive Chairman Hernan Zaballa have navigated the regulatory environment, managed community relationships, overseen technical development, and brought projects through the milestones that matter. This isn’t their first time running this playbook.

The team around him carries similar credentials, including executives and technical advisors with deep experience in Argentine lithium development, brine processing, and project finance.

Management Has Significant Skin in the Game

Here’s the detail that matters most to shareholders: management owns roughly 12% of NOA Lithium Brines increasing to 22% when the rest of the founding group is included.

When insiders hold that much of a company, their incentives are aligned with those of individual investors. They’re not collecting a salary while outside investors take the risk. They win when the stock re-rates and lose if it doesn’t. Additionally, management has demonstrated its commitment by funding the Company when it was needed during difficult periods, and by recently exercising additional warrants.

In a sector full of promotional teams with minimal ownership, that level of insider commitment is impressive.

Here’s a quick recap of why NOA Lithium Brines (TSXV: NOAL); (FSE: N7N); (OTCPK: NLIBF) deserves a closer look right now.

7 Critical Reasons

Why You Should Consider NOA Lithium Brines (TSXV: NOAL); (FSE: N7N); (OTCPK: NLIBF) Today

1

One of the Last High-Grade Lithium Brine Assets of Scale

Most of Argentina’s best lithium salars are already spoken for. What remains is mostly lower-grade, earlier-stage, or locked up under offtakes and royalties. Rio Grande is the exception with 4.7 million tonnes of lithium carbonate equivalent at an average of 525 mg/L, among the highest-grade brine concentrations in Argentina’s area of the Lithium Triangle. That combination of scale and grade is nearly impossible to find today without buying into someone else’s deal. NOA Lithium Brines owns it outright, with no legacy constraints attached.

2

A PEA That Already Points to Billion-Dollar Project Value

Rio Grande is unique because it’s a well-defined asset with impressive economics already on paper. The completed Preliminary Economic Assessment (PEA) outlines a two-stage development with 20,000 tonnes per year initially…before scaling to 40,000 tonnes. At full buildout, the project’s pre-tax net present value approaches $4 billion. Even a single-stage operation points to NPV north of $2 billion. And keep in mind: this is the math on an asset that’s currently trading at a C$70 million market cap. The market is pricing NOA like the PEA doesn’t exist.

3

Peer Valuations Expose a Clear Disconnect

Lithium Chile controls a lower-grade brine resource of around 4 million tonnes in Argentina’s Lithium Triangle. It’s a smaller resource than NOA Lithium Brines’ Rio Grande project…and with lower concentrations that limit its development to Direct Lithium Extraction (DLE) technologies only, with no possibility to use commercially proven evaporation process like the case of NOA Lithium. Yet that company is reportedly under acquisition discussions valuing an 80% stake at $175 million USD. Do the math: that’s three to four times NOA Lithium Brine’s entire market cap, for an inferior asset. NOA Lithium Brines has higher grades, a larger resource, and a completed PEA with billion-dollar economics. Yet it still trades at a fraction of what the market is willing to pay for less. Gaps like this don’t stay open forever.

4

Brine Economics That Work Even When Prices Pull Back

Lithium markets are cyclical. Not every project survives a downturn. That’s where brine assets have a structural edge over hard rock operations thanks to lower capital intensity, lower operating costs and better margins across the cycle. But the advantage goes deeper than cost. Brine projects produce lithium carbonate directly. Hard rock mines in Australia and Africa produce an intermediate concentrate that has to be shipped to China for refining. NOA Lithium Brines’ Rio Grande project doesn’t need elevated prices or a refinery in order to work. That’s the kind of resilience that attracts partners when the market gets selective.

5

Clean Ownership Creates Strategic Flexibility

One of the most underappreciated advantages of NOA Lithium Brines’ Rio Grande project is what it doesn’t have: no legacy offtake agreements, no royalties, no partners or co-owners in any of its projects and no structural constraints that limit the company’s strategic options. That’s rare in Argentina’s lithium sector, where most quality assets already have strings attached. For NOA Lithium Brines, it means full flexibility…no matter if that’s choosing the right development partner, negotiating financing on favorable terms, or positioning for an outright sale. When a major comes looking for high-grade brine exposure, NOA can say yes on its own terms.

6

A Management Team That’s Successfully Done This Before

CEO Gabriel Rubacha has been developing lithium projects in Argentina since the country’s first operation came online in 1997. He was CEO of Minera Exar and President of South American Operations for Lithium Americas. NOA Lithium Brines has a proven leadership team in place with 30 years of experience navigating the exact regulatory, technical, and operational challenges the company will face. Management owns roughly 12% of NOA, which means their incentives are aligned with shareholders and with the rest of the founding group control approximately 22%. Management has been providing funding to the company during difficult periods and has recently exercised additional warrants. When insiders have that much skin in the game, it says something important about the upside potential for the company.

7

Two Additional Salar Assets the Market Isn’t Valuing

Rio Grande is the flagship for NOA Lithium Brines, but it’s not the whole story. NOA also holds 78,000 hectares in the Arizaro salar, representing one of the largest land positions in that salar and an additional 10,000 hectares in the Salinas Grandes salar, with strong infrastructure access. The market is valuing NOA as if only Rio Grande exists. These two projects are essentially free “add-ons”. As Rio Grande advances and attracts attention, Arizaro and Salinas Grandes give NOA additional ways to create value, whether through drilling, partnerships, or spin-off transactions. You’re buying the flagship and getting two district-scale assets thrown in as a bonus.

–

Full Disclaimer:

This website/newsletter is owned, operated and edited by Jade Cabbage Media LLC. Any wording found in this e-mail or disclaimer referencing “I” or “we” or “our” or “Jade Cabbage” refers to Jade Cabbage Media LLC. This webpage/newsletter is a paid advertisement, not a recommendation nor an offer to buy or sell securities. Our business model is to be financially compensated to market and raise awareness for small public companies.

By reading our newsletter and our website you agree to the terms of our disclaimer, which are subject to change at any time. We are not registered or licensed in any jurisdiction whatsoever to provide investing advice or anything of an advisory or consultancy nature and are therefore unqualified to give investment recommendations. Always do your own research and consult with a licensed investment professional before investing. This communication is never to be used as the basis for making investment decisions and is for entertainment purposes only. At most, this communication should serve only as a starting point to do your own research and consult with a licensed professional regarding the companies profiled and discussed. Conduct your own research. Companies with low price per share are speculative and carry a high degree of risk, so only invest what you can afford to lose. By using our service you agree not to hold our site, its editor’s, owners, or staff liable for any damages, financial or otherwise, that may occur due to any action you may take based on the information contained within our newsletters or on our website.

We do not advise any reader to take any specific action. Losses can be larger than expected if the company experiences any problems with liquidity or wide spreads. Our website and newsletter are for entertainment purposes only. Never invest purely based on our alerts. Gains mentioned in our newsletter and on our website may be based on end-of-day or intraday data. This publication and their owners and affiliates may hold positions in the securities mentioned in our alerts, which we may sell at any time without notice to our subscribers, which may have a negative impact on share prices. If we own any shares we will list the information relevant to the stock and number of shares here. The Jade Cabbage Media business model is to receive financial compensation to raise awareness for public companies.

Pursuant to an agreement between Winning Media LLC and NOA Lithium Brines Inc. (NOAL), Winning Media LLC has been hired for a period beginning on 1/19/26 and ending on 4/15/26 to conduct investor relations advertising and marketing and publicly disseminate information about NOA Lithium Brines Inc. (NOAL) via Website, Email and SMS. Winning Media has been compensated the sum total of one hundred fifty thousand dollars via bank wire transfer. Furthermore, Winning Media LLC has paid up to fifteen thousand dollars to Jade Cabbage Media LLC to manage the production budget and digital media campaign for NOA Lithium Brines Inc. (NOAL).

We expect to receive additional compensation as the investor awareness continues. We will disclose every amount we receive. We own zero shares of NOA Lithium Brines Inc. (NOAL). This compensation is a major conflict of interest in our ability to be unbiased regarding. Therefore, this communication should be viewed as a commercial advertisement only.

We have not investigated the background of the hiring party. The third party, profiled company, or their affiliates likely wish to liquidate shares of the profiled company at or near the time you receive this communication, which has the potential to hurt share prices. Any non-compensated alerts are purely for the purpose of expanding our database for the benefit of our future financially compensated investor relations efforts. Frequently companies profiled in our alerts may experience a large increase in volume and share price during the course of investor relations marketing, which may end as soon as the investor relations marketing ceases. Our emails may contain forward-looking statements, which are not guaranteed to materialize due to a variety of factors

We do not guarantee the timeliness, accuracy, or completeness of the information on our site or in our newsletters. The information in our email newsletters and on our website is believed to be accurate and correct, but has not been independently verified and is not guaranteed to be correct. The information is collected from public sources, such as the profiled company’s website and press releases, but is not researched or verified in any way whatsoever to ensure the publicly available information is correct. Furthermore, Jade Cabbage and Winning Media often employs independent contractor writers who may make errors when researching information and preparing these communications regarding profiled companies. Independent writers’ works are double-checked and verified before publication, but it is certainly possible for errors or omissions to take place during editing of independent contractor writer’s communications regarding the profiled company(s). You should assume all information in all of our communications is incorrect until you personally verify the information, and again are encouraged to never invest based on the information contained in our written communications. The information in our disclaimers is subject to change at any time without notice. Please invest carefully and read investment information available at the website of the SEC at http://www.sec.gov.