Sponsored – Est. Read 9 Min

High-Upside Alert:

Potential $920 Million Resource Opportunity Hiding Inside a $75 Million Company

Atlas Salt (TSXV: SALT); (OTCQX: SALQF) appears poised to develop North America’s first new salt mine in 30 years… and it’s already shovel-ready

Right now, one often-overlooked essential resource appears to offer investors a surprising, high-upside opportunity.

That’s because it’s been nearly 30 years since a new salt mine has been built in North America.

Meanwhile, domestic production is shrinking rapidly. Cargill’s historic Avery Island mine shut down permanently in recent years…at a time when demand remains high.

North America now imports an estimated 8 to 10 million tonnes of salt each year from Egypt, Chile and Mexico. That’s a dependency that is both tenuous and increasingly more expensive as shipping costs soar higher.

At exactly the moment when the market desperately needs new domestic capacity, one company has assembled what industry veterans call “the perfect salt project.”

That company is Atlas Salt (TSXV: SALT); (OTCQX: SALQF).

The company’s Great Atlantic Salt Project in Newfoundland, Canada represents the potential for the first new North American salt mine in nearly three decades. With an approved environmental assessment and early permits in hand, it’s shovel-ready and positioned to supply North America’s $3 billion-a-year de-icing market with clean, low-cost, Canadian-made salt.

For investors, the opportunity is impressive:

The company’s 2025 Updated Feasibility Study values the Great Atlantic Salt Project at $920 million NPV8 and 21% IRR and a projected annual free cash flow of $188 million over a 24 year mine life.

Yet Atlas Salt still trades at a market cap of just $75 million.

That’s an 88% valuation discount to the proven economics of a de-risked, construction-ready project.

With project financing as the final step before breaking ground, Atlas Salt offers investors a rare combination of certainty, scarcity and scale and appears poised for a significant potential increase in valuation as it moves into development.

7 CRITICAL REASONS

Why You Should Consider Atlas Salt (TSXV: SALT); (OTCQX: SALQF) Today

1

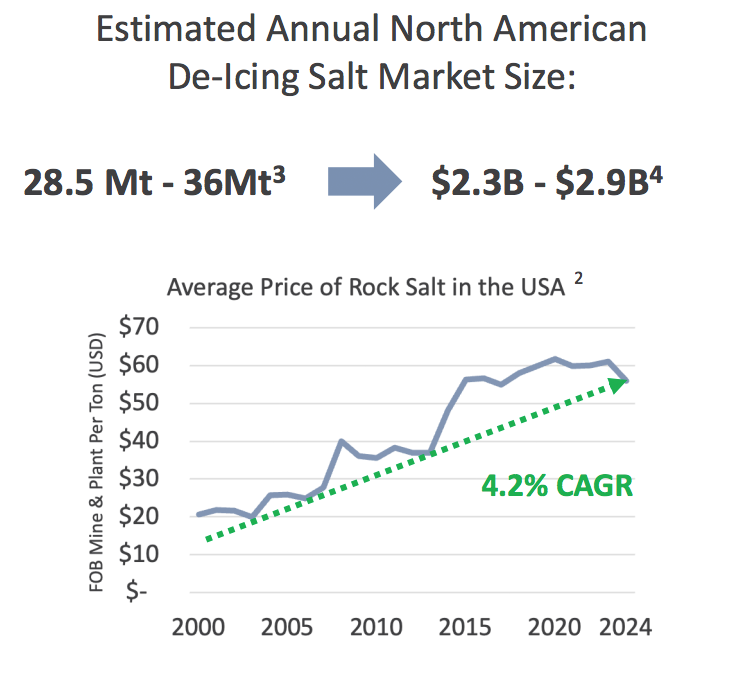

An Overlooked $3 Billion Market That’s Now Facing a Critical Shortage

North America imports up to 10 million tonnes of road salt every year. That’s roughly 30% of total demand…and it comes mostly from Chile and Egypt at a delivered cost that’s climbing every year. And the situation appears to be getting worse, as Cargill’s historic Avery Island mine has already shut down (taking 2.5 million tonnes/year with it) and several other North American mines are forecasted to follow it. With winter demand steady and rising, the continent faces an emerging supply crunch. This rapidly-tightening market creates an enormous opening for a new, efficient, North American supplier…and Atlas Salt (TSXV: SALT); (OTCQX: SALQF) is ready to take full advantage of this opportunity.

2

Atlas Salt Controls a Massive, Strategic Resource in the Perfect Location

Atlas Salt controls the Great Atlantic Salt Project on Newfoundland’s west coast. With 95 million tonnes of reserves, 95.9% purity and 868 million tonnes of inferred resources, the Great Atlantic Salt Project is one of the largest and purest undeveloped salt deposits in North America. The deposit averages 200 meters thick across 3 kilometers. Location is equally perfect as it sits 2 kilometers from a deepwater port, adjacent to the Trans-Canada Highway, and 1.4 kilometers from government-regulated hydroelectric power. While foreign competitors take 14-21 days or more to ship from overseas sources, Atlas Salt offers the ability to deliver clean, Canadian-made salt to Boston, New York or Philadelphia in 3 days.

3

The Great Atlantic Salt Project Is Shovel-Ready, Significantly De-Risked and Built on Proven Economics

Atlas Salt’s Great Atlantic Salt Project is a construction-ready mine one step away from breaking ground. The company has completed its feasibility studies, cleared the environmental assessment process, and received early-works approval from the Newfoundland government. The updated 2025 Feasibility Study shows an after-tax NPV8 of $920 million and a 21.3% IRR, backed by an experienced management team with a track record of building multi-billion-dollar mines. With all major technical, geological, and regulatory hurdles behind it, the only step left before development is securing project financing.

4

Poised to Become North America’s Lowest-Cost Producer By a Wide Margin

At a cost of $34.90 per tonne all-in, Atlas Salt is poised to operate in the bottom quintile of producers worldwide. Legacy competitors are stuck at costs ranging from $60-100+ per tonne thanks to aging infrastructure, soaring energy costs, and hidden legacy environmental issues arising from mines built in a different era. Atlas Salt’s edge is structural: an enclosed modern conveyor eliminates trucks and fuel, hydroelectric power keeps rates stable, battery-electric gear cuts diesel and emissions to zero, and shallow access means no shaft mining is required. Competitors can’t retrofit their projects without building entirely new mines…which is exactly what Atlas Salt is doing. With a $40-50/tonne margin advantage, Atlas Salt would remain profitable as competitors would shutter before they did in any pricing environment.

5

The Time Is Now: Atlas Salt Appears Perfectly Positioned at the Sweet Spot of the Lassonde Curve

In the mining world, the Lassonde Curve maps how valuations rise as projects move from discovery to production. Atlas Salt now sits at the most powerful point on that curve, which is the inflection between feasibility and financing. That’s where de-risked projects invariably experience their fastest potential growth. With environmental approvals secured, economics proven, and financing under active negotiation, Atlas Salt is at the final station before construction. As it transitions from developer to producer, investors could see the kind of multiple expansion that historically drives the biggest gains.

6

Atlas Salt Trades At a Massive Valuation Gap vs. Global Peers

Despite its near-term production potential, Atlas Salt (TSXV: SALT); (OTCQX: SALQF) still trades at an enterprise value of roughly $75 million, compared to $2.5 billion for its only public peer, Compass Minerals. Atlas Salt’s projected Great Atlantic Salt project EBITDA and cashflows would exceed all of Compass Minerals’. A 2022 private-equity deal, led by Stone Canyon, valued producing salt assets held by K+S Group at 13× EBITDA. That’s a metric that implies a potential $4 billion valuation for Atlas at full production, if applied to the Great Atlantic Salt Project’s projected EBITDA. The numbers are hard to ignore: a shovel-ready, fully permitted project with stronger margins than its peers but trading at pennies on the dollar. That disconnect represents a powerful opportunity for early investors.

7

Blue-Sky Expansion: 868 Million Tonnes of “Free” Potential Upside That’s Not Yet Priced In

The current 24-year mine plan is based only on 95 million tonnes of proven and probable reserves. But beneath that lies another 868 million tonnes of high-grade inferred resources, which is nearly nine times the current production plan. As Atlas upgrades and develops those zones, the company could extend the mine’s life well beyond 2050. None of this shows up in today’s $75M valuation. You’re buying a property for the land value and getting a mansion thrown in for free. Early investors get this massive resource upside at zero cost.

A Hidden Supply Crisis Is Rapidly Emerging In One of North America’s Most Essential Materials

For decades, North America has taken its salt supply for granted.

The global salt market (across all applications) was approximately US $25.98 billion in 2024 and is projected to grow to US $36.12 billion by 2032.[i]

Every winter, millions of tonnes of de-icing road salt are spread across highways and city streets to keep traffic moving…but few realize how fragile that supply chain has become.

Domestic production is declining as North American mines that were built decades ago reach the end of their lives as profitable operations.

Operating costs are climbing, environmental liabilities are mounting, and replacement projects are non-existent, Atlas Salt is the only one. Industry analysts now warn that North America is heading into a structural shortage of road salt.

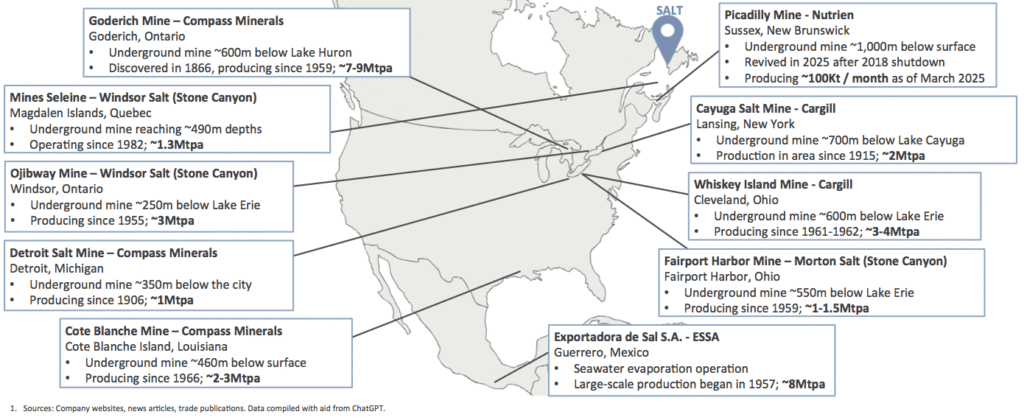

NORTH AMERICA’S TOP PRODUCING SALT MINES

North America’s Legacy Salt Mines Are Old With Many Subjected to Challenging Operating Conditions; Atlas Salt Offers Fresh, Generational, & Relatively Simple Salt Supply For East Coast Markets

Cargill’s historic Avery Island mine in Louisiana has already shut down, removing 2.5 million tonnes of annual supply. Two more Cargill mines in New York and Cleveland remain unsold due to environmental risks. And other North American mining operations face a number of challenges and cost pressures that threaten their immediate future.

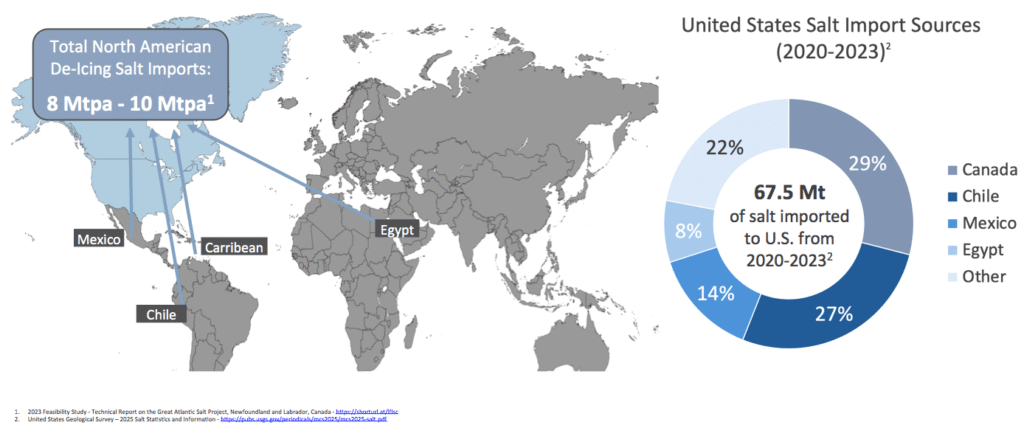

NORTH AMERICA IS RELIANT ON SALT IMPORTS

Great Atlantic Salt’s Planned Production is Easily Absorbed by the Current Market Deficit

Meanwhile, in order to meet demand North America is forced to rely on imports from Chile, Mexico, and Egypt. Those imports accounted for 67.5 million tonnes between 2020 and 2023…but they take weeks to arrive and cost far more to deliver.

As freight rates rise, those imports are becoming both expensive and unreliable.

This is becoming a significant problem as domestic supply is shrinking, demand remains constant, and no new mines are ready to fill the gap.

That’s why Atlas Salt’s timing is extraordinary.

The company brings to the table a shovel-ready project with permits in hand, positioned to bring 4 million tonnes of new capacity online just as the continent’s older mines wind down.

Atlas Salt’s Great Atlantic Salt Project: A World-Class Deposit in Exactly the Right Place

Not all salt deposits are created equal.

Most of the largest sit under lakes and are buried so deep they require costly shafts.

Located on Newfoundland’s west coast near the town of St. George’s, Atlas Salt’s Great Atlantic Salt Project is what geologists call “near-perfect.” That’s because the deposit is shallow, pure, massive, and homogeneous

.

With 95 million tonnes of reserves grading 95.9% NaCl plus 868 million tonnes of inferred resources at 95.2%, Atlas Salt is poised for long-term, profitable production.

With 4Mtpa of nameplate production over its 24.3-year mine life, the project is expected to generate annually an average of:

- $407 million of net revenue…

- $325 million of pre-tax operating cash-flow…

- …and $188 million of post-tax free cash flow each year.

It averages 200 meters thick across 3 kilometers and lies only 180 meters below surface. That’s three times shallower than the world’s largest underground salt mine, Compass Minerals’ Goderich operation, which is approximately 600 meters deep under Lake Huron.

Atlas Salt’s deposit is so shallow it can be accessed via an enclosed conveyor system to continuously move salt from the mine to the nearby marine terminal for immediate shipping. The use of clean hydroelectricity and electric vehicles improves underground safety and minimizes the project’s carbon footprint.

LOCATED IN A TOP-TIER MINING JURISDICTION

Equally important is the project’s location.

The site sits 2 kilometers from the deep-water Turf Point Port, adjacent to the Trans-Canada Highway, and only 1.4 km from a grid-connected hydroelectric substation.

That type of infrastructure would cost hundreds of millions to build from scratch but in the case of the Great Atlantic Salt Project, it already exists.

That logistical advantage means Atlas offers the potential for 3-day shipping to Boston as opposed to 14-21+ days from Egypt or Chile. In other words, Atlas Salt will have the ability to offer lower freight costs, cleaner transport, and faster response to winter surges.

Newfoundland ranks 9th globally in the Fraser Institute’s 2025 mining jurisdiction survey as it is a stable, mining-friendly region that is geopolitically safe.

World-class geology, ideal location, existing infrastructure, and Tier-1 jurisdiction…that’s a powerful combination for Atlas Salt’s Great Atlantic Salt Project.

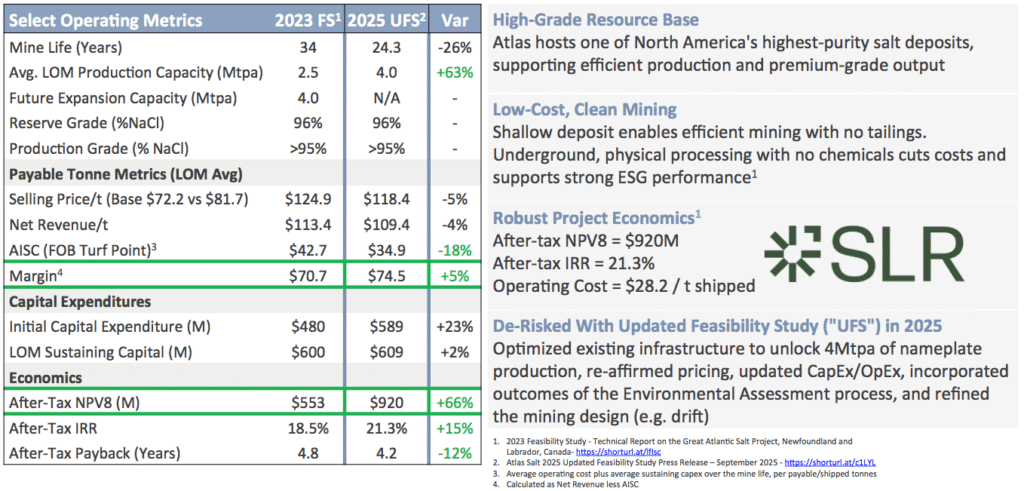

Updated Feasibility Study Could Prove to Be a Game-Changer for Atlas Salt

In September 2025, Atlas Salt released its Updated Feasibility Study on the Great Atlantic Salt Project…and it changed the investment outlook for the project in a powerful way.

The company’s 2023 study already showed strength, in the form of a $553 million after-tax NPV and 18.5% IRR on 2.5 Mtpa production over 34 years.

The 2025 update improved virtually every aspect of the project’s financial outlook:

- After-Tax NPV soared 66% to $920 million…

- After-Tax IRR climbed 270 bps to 21.3%…

- Average Annual Production jumped 63% to 4.0 Mt…

- Mine Life was optimized to 24.3 years (from 34)…

- …and Payback Period was improved to 4.2 years (down from 4.8)

By accelerating production and shortening the mine life, Atlas Salt can now potentially capture more cash flow sooner. This improves the returns for the project and reduces the long-term forecasting risk. The best part is, the significant existing resource (not reserve) represents the high potential for near immediate reserve replenishment. The project has the potential to operate for many more decades than currently contemplated.

SUMMARY OF 2025 UPDATED FEASIBILITY STUDY

The project is now projected to generate $407 million in average annual net revenue…$325 million in pre-tax operating cash flow…and $188 million post-tax free cash flow.

And remember… Atlas Salt (TSXV: SALT); (OTCQX: SALQF) is a company currently trading at a market cap of just $75 million. And we’re talking about the potential for generating $188 million per year in free cash flow once operational.

That’s free cash flow 2.5 times the company’s current valuation…every single year.

This is all driven by the project’s low-cost operations, which call for a life of mine all-in sustaining cost of $34.90/tonne. That puts Atlas Salt in the bottom quintile globally in terms of production cost.

Existing mines face costs of $60 to $100 per tonne with their aging infrastructure while Atlas Salt benefits from its enclosed conveyer system, hydroelectric power, shall access and easy access to more modern infrastructure.

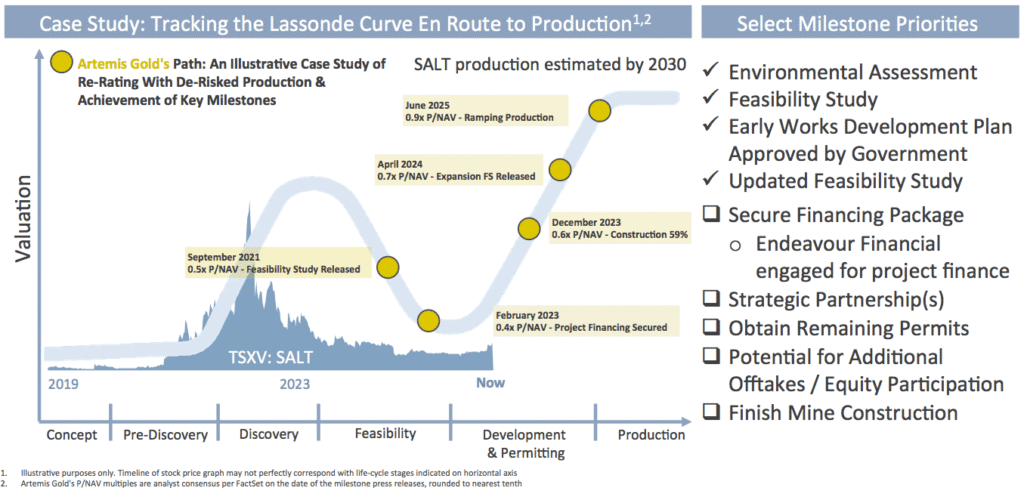

Atlas Salt’s Lassonde Curve Advantage: Why Timing Is Everything

The most successful mining investors understand and live by the Lassonde Curve, which maps how valuations rise through discovery, feasibility, and production.

The sharpest gains typically occur at the inflection between feasibility and financing…the moment when a project becomes real.

That’s precisely where Atlas Salt sits today.

At this stage of the curve, all major uncertainties, such as resource, permits, and environmental approvals, are resolved. The only step left is securing construction financing.

This is when big moves are made…and it’s when institutional investors typically move in. Stocks often re-rate sharply as perception shifts from “speculative” to “near-term producer.”

That’s what happened with Artemis Gold: from feasibility (Sept 2021) to first pour (June 2025), shares rose ~180% as valuation climbed from 0.4× to 0.9× NAV.

POSITIONED FOR RE-RATE & VALUE CREATION

And Atlas Salt (TSXV: SALT); (OTCQX: SALQF) now appears to be in that very same position on the Lassonde Curve.

The company’s Updated Feasibility Study is complete…its Environmental Assessment is approved…its Early Works Permits have been granted…$73 million worth of equipment financing has been arranged…and offtake memorandums of understanding have been secured.

Yet at this critical point on the Lassonde Curve, Atlas Salt trades at just 0.08x NPV, compared with 0.3 to 0.6x NPV for its industry peers.

Even a modest move to the low end of that range – to just 0.3x NPV – would imply 4x upside for the company’s valuation.

The Valuation Disconnect Wall Street Will Eventually Notice

When you compare Atlas Salt’s valuation to its industry peers, something just doesn’t add up.

The company is in control of a world-class asset with superior economics and proven management. Yet the market doesn’t fully understand how to price this into in Atlas’ valuation.

Take a look at Compass Minerals (NYSE: CMP), the only other publicly-traded pure-play salt producer in North America.

Compass Minerals’ enterprise value is currently around CAD $2.5 billion.

But compare their economics to the economic outlook for Atlas Salt at full production:

Atlas: approximately $325M annual EBITDA, $34.90/tonne AISC, 24.3-year mine life, brand new infrastructure, minimal carbon footprint

Compass: approximately $300-320M EBITDA, higher costs, aging operations, declining reserves, diesel-dependent

Atlas has the potential to generate similar or better cash flow from a lower-cost, longer-life, newer mine…yet it trades at just $75 million while Compass trades at $2.5 billion.

That’s a 33x valuation gap.

If Atlas were valued at just 10% of Compass’s enterprise value, which is still a massive discount, the company would be worth $250 million…more than three times today’s price.

As you can see…the upside is significant.

Another comparable is a recent private equity transaction. In 2021, Stone Canyon Industries acquired K+S’s North and South American salt business for US $3.2 billion. K+S was generating roughly US$250 million annual EBITDA, which implies 13x EBITDA.

Apply that 13x to Atlas’s projected CAD $325M EBITDA and you get a potential CAD $4.2 billion valuation…which is more than 50 times the current market cap.

Even with a 50-75% discount for being pre-production, fair value is $1-2 billion, or 15-25x higher than today.

Atlas Salt’s Green Advantage Competitors Can’t Match

Another important consideration for Atlas Salt is that the company is building in all likelihood the cleanest mining operation on the planet.

The company’s projected emissions are just 79 tonnes of CO₂ a year[i], which is roughly the same as four Newfoundland households. That’s about 99% lower than a typical mine.

This is happening because the Great Atlantic Salt Project runs on clean hydroelectric power and uses all-electric equipment underground. There’s no processing plant, no tailings, and no diesel trucks rumbling to the port.

There’s just an enclosed conveyor that moves salt straight to the ship.

Why does that matter for investors?

It means that Atlas is potentially protected as carbon regulations tighten, can attract ESG-focused capital that competitors can’t, and will appeal to those customers who increasingly prefer low-carbon suppliers.

Even a small “green premium” of just $5 per tonne could add about $20 million in revenue every year, which can add up to nearly half a billion dollars over the mine’s life.

[i] Source: 2025 feasibility study

Atlas Salt is Led By An Experienced Team… With Serious Skin in the Game

In the mining world, leadership makes or breaks companies.

In the case of Atlas Salt, management is both proven and personally invested…and that’s an important consideration.

The company is led by a management team with proven track records advancing large-scale mining projects…and cumulative experience developing more than $3 billion in mining assets from feasibility through production.

CEO Nolan Peterson brings over 20 years of experience in mine development, operations, and finance and is the former CEO of World Copper, advancing $1B+ in assets.

CFO Jeffrey Kilborn has 20+ years in mining finance and capital markets and is the former CFO of Canadian Gold Corp. He’s structured deals that protect shareholder value while securing capital.CEO Nolan Peterson brings over 20 years of experience in mine development, operations, and finance and is the former CEO of World Copper, advancing $1B+ in assets.

VP Engineering & Construction Robert Booth delivered $1.5B+ in mine builds for Newmont, Vale and Hudbay over 30+ years. He’ll oversee Atlas’s transition from drawings to actual infrastructure…and he’s done it successfully before.

Project Director Andrew Smith brings 10+ years underground mine construction, most recently leading $500M+ in projects as Head of PMO at Dumas Contracting.

Those credentials are impressive…but credentials only matter if management is personally invested.

With Atlas Salt, insider ownership exceeds 40%.

Management and board own more than 40 million shares…or roughly two-fifths of the company. Their personal wealth rises or falls with the stock price just like any shareholder and like any other shareholder many of them have bought and continue to buy in the open market.

This isn’t a team collecting salaries while retail takes the risk. When management owns 40%+, incentives are perfectly aligned. They can’t get rich unless shareholders get rich.

And this team has already delivered: They’ve guided Atlas through a decade of work that has led them to be the only salt development story on the continent. They’ve completed drill programs, navigated environmental assessments, delivered two feasibility studies, secured strategic partnerships, and reached shovel-ready status.

7 CRITICAL REASONS

Why You Should Consider Atlas Salt (TSXV: SALT); (OTCQX: SALQF) Today

1

An Overlooked $3 Billion Market That’s Now Facing a Critical Shortage

North America imports up to 10 million tonnes of road salt every year. That’s roughly 30% of total demand…and it comes mostly from Chile and Egypt at a delivered cost that’s climbing every year. And the situation appears to be getting worse, as Cargill’s historic Avery Island mine has already shut down (taking 2.5 million tonnes/year with it) and several other North American mines are forecasted to follow it. With winter demand steady and rising, the continent faces an emerging supply crunch. This rapidly-tightening market creates an enormous opening for a new, efficient, North American supplier…and Atlas Salt (TSXV: SALT); (OTCQX: SALQF) is ready to take full advantage of this opportunity.

2

Atlas Salt Controls a Massive, Strategic Resource in the Perfect Location

Atlas Salt controls the Great Atlantic Salt Project on Newfoundland’s west coast. With 95 million tonnes of reserves, 95.9% purity and 868 million tonnes of inferred resources, the Great Atlantic Salt Project is one of the largest and purest undeveloped salt deposits in North America. The deposit averages 200 meters thick across 3 kilometers. Location is equally perfect as it sits 2 kilometers from a deepwater port, adjacent to the Trans-Canada Highway, and 1.4 kilometers from government-regulated hydroelectric power. While foreign competitors take 14-21 days or more to ship from overseas sources, Atlas Salt offers the ability to deliver clean, Canadian-made salt to Boston, New York or Philadelphia in 3 days.

3

The Great Atlantic Salt Project Is Shovel-Ready, Significantly De-Risked and Built on Proven Economics

Atlas Salt’s Great Atlantic Salt Project is a construction-ready mine one step away from breaking ground. The company has completed its feasibility studies, cleared the environmental assessment process, and received early-works approval from the Newfoundland government. The updated 2025 Feasibility Study shows an after-tax NPV8 of $920 million and a 21.3% IRR, backed by an experienced management team with a track record of building multi-billion-dollar mines. With all major technical, geological, and regulatory hurdles behind it, the only step left before development is securing project financing.

4

Poised to Become North America’s Lowest-Cost Producer By a Wide Margin

At a cost of $34.90 per tonne all-in, Atlas Salt is poised to operate in the bottom quintile of producers worldwide. Legacy competitors are stuck at costs ranging from $60-100+ per tonne thanks to aging infrastructure, soaring energy costs, and hidden legacy environmental issues arising from mines built in a different era. Atlas Salt’s edge is structural: an enclosed modern conveyor eliminates trucks and fuel, hydroelectric power keeps rates stable, battery-electric gear cuts diesel and emissions to zero, and shallow access means no shaft mining is required. Competitors can’t retrofit their projects without building entirely new mines…which is exactly what Atlas Salt is doing. With a $40-50/tonne margin advantage, Atlas Salt would remain profitable as competitors would shutter before they did in any pricing environment.

5

The Time Is Now: Atlas Salt Appears Perfectly Positioned at the Sweet Spot of the Lassonde Curve

In the mining world, the Lassonde Curve maps how valuations rise as projects move from discovery to production. Atlas Salt now sits at the most powerful point on that curve, which is the inflection between feasibility and financing. That’s where de-risked projects invariably experience their fastest potential growth. With environmental approvals secured, economics proven, and financing under active negotiation, Atlas Salt is at the final station before construction. As it transitions from developer to producer, investors could see the kind of multiple expansion that historically drives the biggest gains.

6

Atlas Salt Trades At a Massive Valuation Gap vs. Global Peers

Despite its near-term production potential, Atlas Salt (TSXV: SALT); (OTCQX: SALQF) still trades at an enterprise value of roughly $75 million, compared to $2.5 billion for its only public peer, Compass Minerals. Atlas Salt’s projected Great Atlantic Salt project EBITDA and cashflows would exceed all of Compass Minerals’. A 2022 private-equity deal, led by Stone Canyon, valued producing salt assets held by K+S Group at 13× EBITDA. That’s a metric that implies a potential $4 billion valuation for Atlas at full production, if applied to the Great Atlantic Salt Project’s projected EBITDA. The numbers are hard to ignore: a shovel-ready, fully permitted project with stronger margins than its peers but trading at pennies on the dollar. That disconnect represents a powerful opportunity for early investors.

7

Blue-Sky Expansion: 868 Million Tonnes of “Free” Potential Upside That’s Not Yet Priced In

The current 24-year mine plan is based only on 95 million tonnes of proven and probable reserves. But beneath that lies another 868 million tonnes of high-grade inferred resources, which is nearly nine times the current production plan. As Atlas upgrades and develops those zones, the company could extend the mine’s life well beyond 2050. None of this shows up in today’s $75M valuation. You’re buying a property for the land value and getting a mansion thrown in for free. Early investors get this massive resource upside at zero cost.

[1] https://www.fortunebusinessinsights.com/salt-market-103011

[1] Source: 2025 feasibility study

Full Disclaimer:

This website/newsletter is owned, operated and edited by Jade Cabbage Media LLC. Any wording found in this e-mail or disclaimer referencing “I” or “we” or “our” or “Jade Cabbage” refers to Jade Cabbage Media LLC. This webpage/newsletter is a paid advertisement, not a recommendation nor an offer to buy or sell securities. Our business model is to be financially compensated to market and raise awareness for small public companies.

By reading our newsletter and our website you agree to the terms of our disclaimer, which are subject to change at any time. We are not registered or licensed in any jurisdiction whatsoever to provide investing advice or anything of an advisory or consultancy nature and are therefore unqualified to give investment recommendations. Always do your own research and consult with a licensed investment professional before investing. This communication is never to be used as the basis for making investment decisions and is for entertainment purposes only. At most, this communication should serve only as a starting point to do your own research and consult with a licensed professional regarding the companies profiled and discussed. Conduct your own research. Companies with low price per share are speculative and carry a high degree of risk, so only invest what you can afford to lose. By using our service you agree not to hold our site, its editor’s, owners, or staff liable for any damages, financial or otherwise, that may occur due to any action you may take based on the information contained within our newsletters or on our website.

We do not advise any reader to take any specific action. Losses can be larger than expected if the company experiences any problems with liquidity or wide spreads. Our website and newsletter are for entertainment purposes only. Never invest purely based on our alerts. Gains mentioned in our newsletter and on our website may be based on end-of-day or intraday data. This publication and their owners and affiliates may hold positions in the securities mentioned in our alerts, which we may sell at any time without notice to our subscribers, which may have a negative impact on share prices. If we own any shares we will list the information relevant to the stock and number of shares here. The Jade Cabbage Media business model is to receive financial compensation to raise awareness for public companies.

Pursuant to an agreement between Winning Media LLC and the issuer, Atlas Salt Inc. (SALT), Winning Media LLC has been hired for a period beginning on 11/03/25 and ending on 12/12/25 to conduct investor relations advertising and marketing and publicly disseminate information about Atlas Salt Inc. (SALT) via Website, Email and SMS. Winning Media has been compensated the sum total of fifty thousand dollars via bank wire transfer. Furthermore, Winning Media LLC has paid up to fifteen thousand dollars to Jade Cabbage Media LLC to manage the production budget and digital media campaign for Atlas Salt Inc. (SALT).

We expect to receive additional compensation as the investor awareness continues. We will disclose every amount we receive. We own zero shares of Atlas Salt Inc. (SALT). This compensation is a major conflict of interest in our ability to be unbiased regarding. Therefore, this communication should be viewed as a commercial advertisement only.

We have not investigated the background of the hiring party. The third party, profiled company, or their affiliates likely wish to liquidate shares of the profiled company at or near the time you receive this communication, which has the potential to hurt share prices. Any non-compensated alerts are purely for the purpose of expanding our database for the benefit of our future financially compensated investor relations efforts. Frequently companies profiled in our alerts may experience a large increase in volume and share price during the course of investor relations marketing, which may end as soon as the investor relations marketing ceases. Our emails may contain forward-looking statements, which are not guaranteed to materialize due to a variety of factors

We do not guarantee the timeliness, accuracy, or completeness of the information on our site or in our newsletters. The information in our email newsletters and on our website is believed to be accurate and correct, but has not been independently verified and is not guaranteed to be correct. The information is collected from public sources, such as the profiled company’s website and press releases, but is not researched or verified in any way whatsoever to ensure the publicly available information is correct. Furthermore, Jade Cabbage and Winning Media often employs independent contractor writers who may make errors when researching information and preparing these communications regarding profiled companies. Independent writers’ works are double-checked and verified before publication, but it is certainly possible for errors or omissions to take place during editing of independent contractor writer’s communications regarding the profiled company(s). You should assume all information in all of our communications is incorrect until you personally verify the information, and again are encouraged to never invest based on the information contained in our written communications. The information in our disclaimers is subject to change at any time without notice. Please invest carefully and read investment information available at the website of the SEC at http://www.sec.gov.